The assessment, analysis, and strategic imperatives in this report are powered by Nexstrat.ai. To experience live how Nexstrat.ai empowers your business in strategy development and decisions, book a demo at nexstrat.ai/book-a-demo.

Introduction

The energy sector in the GCC is at a critical crossroads. In 2023–2024, oil giants and national oil companies (NOCs) are not only maximizing near-term hydrocarbon production but also accelerating the transition to cleaner, more sustainable energy systems. Fueled by record oil revenues, governments across Saudi Arabia, the UAE, Qatar, and beyond have embarked on ambitious projects to secure energy security while positioning themselves as global leaders in renewables. Massive capital expenditures are being channeled into traditional oil & gas infrastructure—even as plans for renewable projects, green hydrogen, and petrochemicals are gaining momentum. Amid these shifts, energy executives face a dual challenge: to balance the enduring legacy of hydrocarbons with the pressing need for a clean-energy future.

Government policies are evolving rapidly: new net‑zero targets, revamped subsidies, and strategic reforms are laying the groundwork for an integrated energy ecosystem. At the corporate level, energy majors like Saudi Aramco and ADNOC are leveraging their robust balance sheets to push forward with both expansion and diversification. Investments in petrochemicals and clean tech are now seen as essential hedges against the long‑term decline in oil demand, while state‑backed financing is fueling large‑scale projects that promise to reshape the region’s energy profile.

The transformation is not without risk. Oil price volatility, execution challenges in mega-projects, and the race to secure talent and technology all pose significant hurdles. Yet, the opportunities are equally compelling: from emerging green energy export markets and carbon capture initiatives to the promise of integrated energy solutions that combine traditional oil with renewables. In this dynamic landscape, energy leaders must adopt a forward‑looking strategy that not only protects against downside risks but also capitalizes on the inevitable energy transition.

Booming Investments and Policy Shifts:

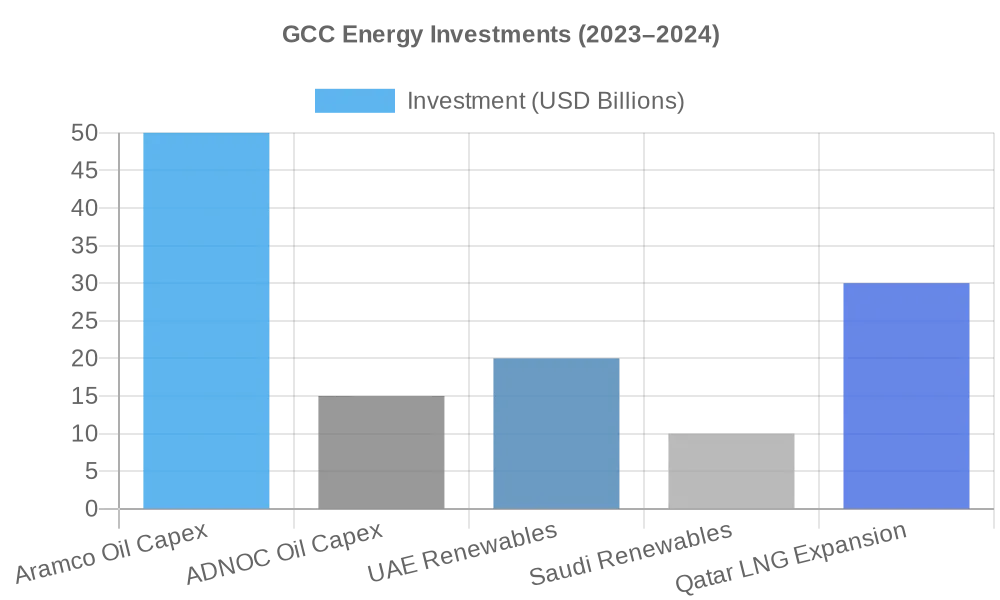

The energy sector remains the backbone of GCC economies, but 2023–24 saw a dual mandate: maximize near-term oil/gas output and accelerate the energy transition. Saudi Arabia and the UAE – the region’s biggest producers – are both expanding oil production capacity with unprecedented capital outlays. Abu Dhabi’s ADNOC, for instance, approved a AED 550 billion ($150 billion) CAPEX for 2023–2027 to boost oil capacity to 5 million barrels/day by 2027 (pulled forward from 2030) (reuters.com)

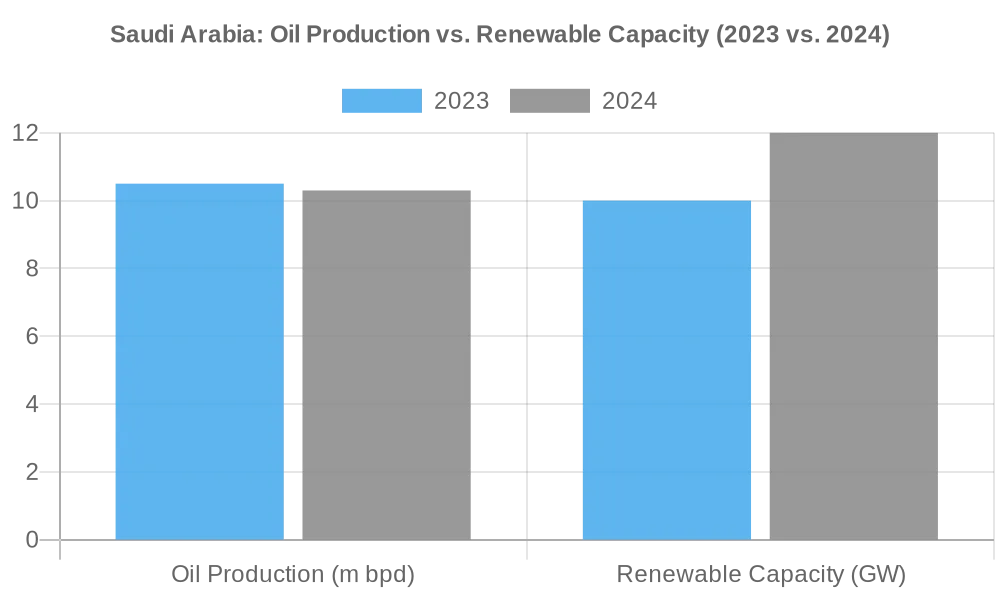

Saudi Aramco likewise set a record annual CAPEX (targeting $45–55 billion in 2023) to sustain 12 million bpd capacity and develop major new gas fields (aramco.com.) At the same time, all GCC governments have announced net-zero emissions targets (UAE by 2050, Saudi by 2060, etc.) and rolled out renewable energy strategies. The numbers are striking: Saudi Arabia aims for 58.7 GW of renewables by 2030, up from only ~10 GW under development currently, implying a massive ramp-up of solar and wind projects (pwc.com.) Across the GCC, renewables still accounted for just 3% of power capacity as of 2022, but investments are now soaring – the UAE alone represents 70% of the region’s renewable capacity and investment to date (irena.org )

Following the UAE’s high-profile hosting of COP28 in late 2023, green initiatives have gained further momentum. Governments are reforming energy subsidies and setting clean energy targets (e.g. UAE’s Energy Strategy 2050 calls for 50% clean power by 2050) to curb domestic oil consumption and free up resources for export. (pwc.com) They are also positioning the region as a hub for sustainable finance – Abu Dhabi Global Market launched the world’s first regulated carbon-credit trading exchange in partnership with AirCarbon, aligning finance with climate goals. (pwc.com) In sum, energy policy is now a two-track effort: ensure oil market stability and monetization today, while investing petrodollars into the low-carbon industries of tomorrow.

Corporate Strategy – NOCs Pivot and Diversify:

GCC national oil companies are adapting to this mandate with aggressive strategies.

Oil & Gas Expansion:

Despite softer crude prices in 2023 versus 2022, upstream investments remain full-steam. Aramco and ADNOC are leveraging strong balance sheets to finance growth – S&P forecasts oil, gas and chemicals firms in the GCC energy sector will increase EBITDA by ~5–10% over the next two years as new production comes online.(spglobal.com) Both firms are also bolstering natural gas: Aramco raised its gas output target 60% by 2030 (vs 2021 levels) to supply power and industrial growth (aramco.com).

QatarEnergy, for its part, is deep into a $30+ billion expansion of North Field LNG capacity (set to boost LNG output ~64% by 2027), securing long-term supply deals with Asian and European buyers.

Downstream and Petrochemicals:

Anticipating long-term threats to fuel demand, Gulf NOCs in the GCC energy sector are moving down the value chain. Aramco invested more than $100 billion in petrochemicals projects this decade to make downstream as prominent as upstream (aa.com.tr). – in 2023 it acquired a 10% stake in China’s Rongsheng Petrochemical and commenced building large refining-chemicals complexes in China (pwc.com). Aramco’s CEO noted the company is “positioning for a future in which oil and gas remain key for decades alongside new energy solutions,” highlighting ongoing mega-projects in crude-to-chemicals conversion and overseas refining (aramco.com). ADNOC likewise merged its gas processing & LNG units into a new ADNOC Gas subsidiary and floated a minority stake in 2023, raising capital to fund expansion (reuters.com). It also created a dedicated “Low Carbon Solutions & International Growth” division focused on cleaner energy, gas, LNG and chemicals, and pledged $15 billion for decarbonization projects by 2030 (reuters.com).

Renewables and Hydrogen:

Oil companies in the GCC energy sector are increasingly backing renewable ventures (often via partnerships). Saudi ACWA Power (part-owned by PIF and Saudi Aramco) is building giga-scale solar and green hydrogen plants (e.g. the NEOM Green Hydrogen project slated for 2026). Aramco signed deals to develop 2.66 GW of solar capacity in 2023 (aramco.com). and ADNOC is investing in UAE’s 5 GW offshore wind plans and exploring blue ammonia exports. All GCC states are eyeing leadership in hydrogen – UAE and Oman have issued hydrogen roadmaps, and Saudi Arabia made its first trial shipments of blue ammonia to Asia.

Emerging Players:

It’s not just state giants; private and semi-private players are adapting too. Utilities and industry players inthe GCC energy sector (e.g. UAE’s Masdar, Oman’s OQ, and ENGIE’s regional JV) are scaling up renewable generation. New specialty firms are springing up in carbon capture and storage (CCS) technology, leveraging the region’s geological storage potential and oil EOR needs. Across the board, the traditional oil-and-gas business model is broadening into an “integrated energy” model spanning hydrocarbons, renewables, and value-added products.

Key Risks:

While the outlook is robust, energy executives face a complex risk landscape.

Oil Market Volatility:

OPEC+ production cuts kept oil around $80 in 2023, but any collapse in prices (due to global recession or geopolitical shocks) could quickly shrink government spending and delay projects. The risk of overcapacity is also real – if multiple GCC producers and others (e.g. US shale) expand simultaneously, supply could overshoot demand mid-decade. Companies like S&P note that a drop below ~$85/barrel would erode utilization and margins for oilfield service firms and upstream ventures (spglobal.com).

Energy Transition Uncertainty:

There is execution risk in the pivot to new energies – renewables still contribute marginally, and projects can face delays (e.g. grid infrastructure, supply chain lags for solar components). If global climate policies tighten faster than expected, long-lived oil assets might face demand risk or stranded asset risk. Conversely, if the energy sector in GCC doesn’t diversify quickly enough, it could be left with obsolete infrastructure in a decarbonizing world.

Regulatory and ESG Pressure:

Hosting COP28 put a spotlight on GCC climate action. Public scrutiny of “greenwashing” is high – e.g. ADNOC’s COP28 role drew criticism (reuters.com). Companies must navigate evolving ESG reporting standards and possibly carbon pricing mechanisms at home.

Talent and Capacity Constraints:

A more immediate internal risk is the sheer volume of simultaneous projects. The “war for talent” in GCC is intensifying as each country localizes its workforce and mega-projects proliferate (pwc.com). Specialized engineers, project managers, and technicians are in short supply, potentially causing cost inflation and delays. Supply chains for materials (steel, cement, drilling equipment) are stretched by the construction boom, raising procurement and execution risks. Finally, geopolitical tensions in the broader Middle East (e.g. conflicts affecting shipping lanes in the Red Sea or Gulf) remain a perennial risk to energy exports and infrastructure (agbi.com), though the GCC itself has been a zone of relative stability.

Overlooked Opportunities:

Despite risks, new opportunities are emerging.

Green Energy Exports:

The GCC could become a major exporter not only of oil, but of solar electricity (via undersea cable projects) and green hydrogen/ammonia to energy-hungry markets in Europe and Asia. Early investments in hydrogen (as planned in NEOM and Oman) could capture significant market share in future clean fuel trade.

Carbon Management: Gulf companies can leverage their scale to lead in carbon capture and storage (CCS) and carbon markets. ADNOC and Aramco’s expertise in injecting CO₂ for enhanced oil recovery can evolve into large-scale CO₂ sequestration services – a business line if global carbon prices rise. Abu Dhabi’s planned carbon exchange in ADGM is an example of monetizing this opportunity (pwc.com).

Downstream Value-Add:

There is untapped potential in converting more of the region’s hydrocarbons into petrochemicals, plastics, and even specialty products (e.g. hydrogen-derived fertilizers, synthetic fuels). By investing in R&D and advanced refining, GCC firms can climb the value chain and reduce exposure to crude price swings.

Regional Energy Trade: GCC states are also starting to interconnect – the GCC power grid is being upgraded, and Saudi is exporting electricity to neighbors. A more integrated regional energy grid could improve efficiency and allow sale of excess renewable power across borders.

Public-Private Partnerships: Lastly, the push for renewables opens space for private investment. Governments are tendering solar/wind projects on IPP models (as seen with Saudi’s Sakaka solar park and UAE’s Al Dhafra PV project). This is drawing international developers and creating a more dynamic energy ecosystem beyond just state monopolies.

Strategic Imperatives for Energy Sector Leaders:

- Diversify for Resilience: Reinvest current oil windfalls into future-proof assets. Double down on downstream integration and renewables to hedge against long-term declines in oil demand (aramco.com)(irena.org). For example, allocate capital to petrochemical complexes, utility-scale solar/wind farms, and gas value chains (LNG, hydrogen) – these will be pillars of the business in the 2030s.

- Innovate in Low-Carbon Solutions: Don’t treat the energy transition as a compliance task; make it a competitive advantage. Invest in carbon capture, hydrogen production, and energy efficiency technologies now, while funding is ample. Early movers can lock in technology partnerships and shape emerging markets (e.g. become the Gulf’s leading blue ammonia exporter) (reuters.com). Aim to meet national carbon targets profitably – e.g. by monetizing captured CO₂ or trading offset credits on platforms like the ADGM exchange (pwc.com).

- Strengthen Partnerships and Supply Chains: Given the scale of projects, collaborate strategically. Form JV alliances with global tech leaders (for renewable tech, AI-driven exploration, etc.) to access know-how and spread risk. Also coordinate with government initiatives – for instance, align refinery upgrades with national petrochemicals strategies, or co-develop training programs with ministries to alleviate talent gaps. On supply chains, secure critical materials via long-term contracts and consider localizing production of key inputs (pipes, solar panels) to reduce import bottlenecks.

- Talent Development and Productivity: The human capital challenge is real – winning in the new energy era requires top-notch expertise across oil, gas, and renewables. CEOs should invest in workforce development, from upskilling national engineers to attracting global experts with competitive packages. Build in-house training centers or partnerships with universities (e.g. research on carbon capture or battery tech) to create a pipeline of skills. Simultaneously, boost productivity through digital tools – deploy AI, IoT and advanced analytics in operations to do more with a leaner workforce. This not only offsets talent shortages but also improves safety and efficiency.

- Robust Risk Management: Finally, navigate volatility with rigorous planning. Conduct scenario analyses for oil price swings and carbon regulation impacts, and maintain financial discipline on projects (to avoid overstretch if conditions change). Strengthen cybersecurity around critical energy infrastructure in light of increasing digitalization and regional cyber threats. By institutionalizing risk management and agility (for example, the ability to scale capex up or down quickly), energy companies can remain profitable through the sector’s inevitable cycles.

Explore more insights in our blogs on NexStrat.AI.

About NexStrat AI:

NexStrat AI is at the forefront of AI and business strategy innovation. As the ultimate strategy and transformation AI co-pilot and platform, we help leaders and strategists craft winning strategies and make effective decisions with speed and confidence.

Contact Us:

Have questions or want to learn more? Contact us at [email protected]

Follow Us:

Join our community of forward-thinking business leaders on LinkedIn.