Introduction: The Pulse of Power in March 2025

As of March 2025, the US financial sector stands at a pivotal juncture. The economy is advancing at a projected 2.4% GDP growth rate, with inflation stabilized at 2.3%, and the Federal Reserve’s recent rate reductions are catalyzing renewed lending activity. For CEOs and boards in finance, this environment presents not merely a period of stability but a call to action. The past two years—marked by 2023’s high interest rate pressures and 2024’s accelerated digital transformation—have set the stage for a profound shift in financial sector strategy. Bank lending is projected to rise by 3-4%, investments in artificial intelligence (AI) are growing at 25% annually, and emerging regulatory signals suggest a potential acceleration in cryptocurrency adoption. This article explores these dynamics, their strategic implications, and the imperatives for leadership to shape the sector’s future trajectory.

Macroeconomic Context: Resilience Amid Transformation

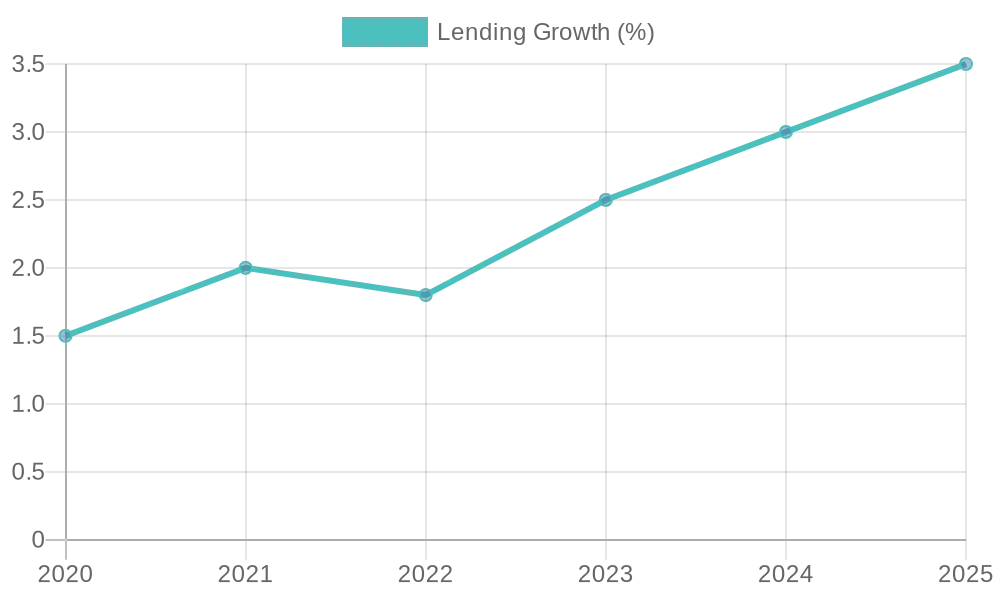

The financial sector’s journey through 2023 and 2024 provides critical context. In 2023, elevated interest rates compressed net interest margins, as detailed in the FDIC’s Quarterly Banking Profile, challenging traditional revenue models. By 2024, the Federal Reserve’s shift to rate cuts spurred a recovery, with early 2025 data indicating a 3-4% increase in bank lending, driven by improved consumer and business borrowing conditions. Concurrently, AI has emerged as a transformative force requiring a fundamentally different approach to financial sector strategy . Investments reached $100 billion in 2024, enabling institutions to enhance risk management and customer engagement—evidenced by a 30% reduction in fraud detection times at leading banks.

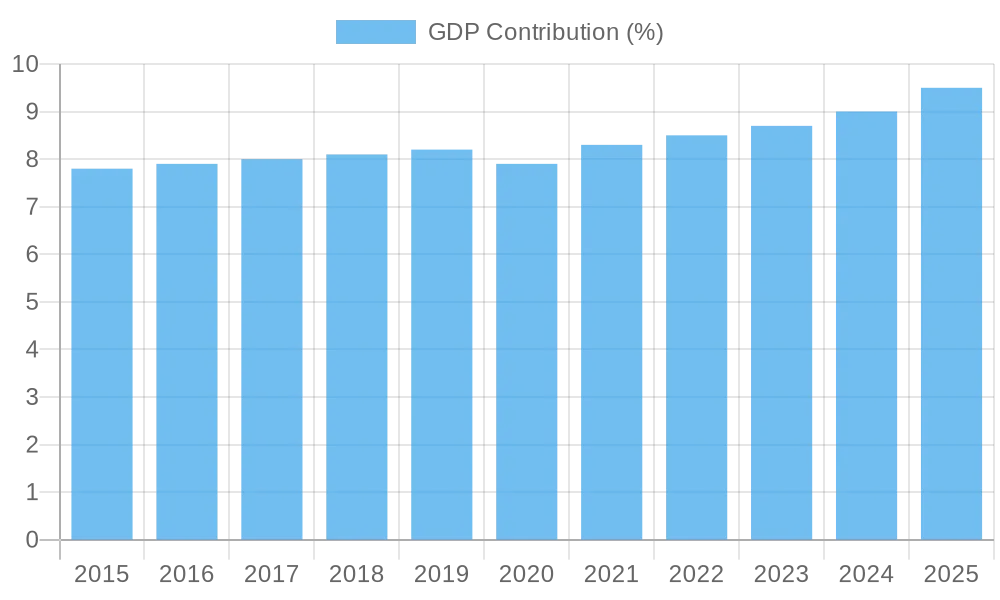

Cryptocurrency represents another frontier. Following a restrictive regulatory environment in 2023, Freshfields highlights potential leadership changes at the SEC and CFTC that could facilitate broader adoption by mid-2025. The sector’s contribution to GDP, consistently at 8-10%, is poised for further growth as digital assets gain traction. These trends are illustrated below:

Forces Reshaping the Sector

Beyond these headline trends, deeper currents are at play. AI’s impact extends past operational efficiency into strategic differentiation. EY forecasts that institutions adopting proprietary AI models could reduce operating costs by 20% by 2026, leveraging decades of transactional data to predict defaults with over 90% accuracy. Simultaneously, partnerships with FinTech firms have surged, with Deloitte noting a 15% increase in collaborations in 2024, targeting innovations such as alternative credit scoring and micro-investing platforms.

Cryptocurrency’s evolution merits close attention. PwC reports a 71% rise in financial services M&A deal values in 2024, driven by investments in blockchain infrastructure. A mid-sized bank acquiring a crypto custody provider could secure an immediate foothold in a market projected to reach $2 trillion by 2030. However, regulatory uncertainty remains a critical variable—JPMorgan suggests that a restrictive stance could delay widespread adoption by 18 months, while a permissive shift might see 10% of US banks offering crypto services by 2027.

Strategic Implications:

Key Risks:

The financial sector in 2025 confronts a complex array of risks that could reshape its trajectory and strategy. Regulatory uncertainty surrounding cryptocurrency looms large—PwC notes that the pace and direction of policy evolution, potentially influenced by leadership changes at the SEC and CFTC, remain unpredictable. A restrictive regulatory posture could stifle the sector’s ability to capitalize on digital assets, locking institutions into legacy models while competitors in less regulated markets gain ground.

Conversely, a rapid shift toward permissiveness might overwhelm existing compliance frameworks, exposing firms to legal vulnerabilities and reputational damage as they scramble to adapt. Cybersecurity emerges as an equally pressing concern—IBM highlights the growing sophistication of AI-driven attacks, which could exploit vulnerabilities in newly deployed systems. Such breaches threaten not only operational continuity but also the trust of clients and regulators, amplifying the stakes in an era of heightened scrutiny.

Macroeconomic fragility adds another layer of risk—Conference Board data showing tepid job growth in early 2025 signals potential softening in consumer confidence, which could curtail lending activity and undermine the sector’s recovery from 2023’s high-rate environment.

Key Considerations:

Navigating this financial landscape demands a shift in strategy that balances bold innovation with operational resilience. The integration of AI into core functions—such as risk assessment, fraud detection, and customer personalization—requires careful calibration. McKinsey underscores that while AI can streamline processes and uncover insights from vast datasets, an overzealous push toward automation risks eroding the human relationships that remain vital in high-value segments like wealth management or complex commercial lending.

Leaders must weigh the trade-offs between efficiency gains and the preservation of client trust, crafting a hybrid model that leverages technology without sacrificing the nuanced judgment humans provide. Interest rate dynamics, still reverberating from 2023’s tightening cycle, further complicate strategic planning—JPMorgan suggests that volatility could persist, necessitating flexible treasury strategies that adapt to shifting conditions rather than relying on fixed assumptions.

Partnerships with FinTech firms, increasingly central to innovation as per Deloitte, demand discernment—prioritizing collaborators with unique, data-driven capabilities over those offering commoditized solutions can unlock new revenue streams, but missteps could dilute focus and strain resources.

Key Opportunities:

Amid these challenges lie significant opportunities for strategic differentiation. Wealth management stands out as a domain ripe for reinvention—US Bank observes that younger, tech-savvy investors are driving demand for personalized, AI-enhanced solutions that traditional models struggle to deliver. Institutions that pioneer seamless, technology-enabled experiences could capture this growing segment, redefining client relationships for the next decade.

Digital banking offers a parallel avenue, particularly for engaging demographics underserved by conventional channels—platforms that have thrived since 2020 demonstrate the potential to build loyalty through convenience and accessibility.

Cryptocurrency, contingent on regulatory evolution, represents a transformative frontier—Freshfields suggests that a favorable policy shift could position early adopters as market leaders, leveraging blockchain to offer innovative services like custody or trading. Strategic alliances with FinTechs, when executed with precision, can accelerate this transformation, bypassing the inertia of legacy systems and delivering capabilities that redefine competitive boundaries.

Strategic Imperatives: A Roadmap for 2025 and Beyond

Leverage AI for Competitive Advantage:

The transformative potential of artificial intelligence (AI) demands a focused strategy on embedding it deeply into core financial operations, beyond superficial enhancements. EY underscores that AI’s value lies in its ability to unlock insights from vast datasets—such as transactional histories or customer interactions—enabling proactive risk management and tailored client experiences. Leaders must prioritize the development of proprietary AI capabilities over generic solutions, crafting systems that reflect the institution’s unique market position and client needs.

This approach requires a commitment to integrating AI with human expertise, ensuring that automation enhances rather than supplants the nuanced decision-making critical to high-value relationships, such as in wealth management or complex lending. The imperative here is to position AI as a differentiator, driving efficiency and foresight while preserving the trust that underpins long-term client loyalty.

Strengthen Cybersecurity Resilience: In an era where digital transformation accelerates exposure, cybersecurity must evolve from a defensive necessity to a strategic enabler. Capco warns of emerging threats, including those posed by quantum computing advancements, which could challenge existing security frameworks. This imperative calls for a proactive stance—building robust, AI-enhanced defenses that anticipate and neutralize sophisticated attacks before they materialize.

Leaders should focus on fostering a culture of resilience, embedding security into every layer of operations, from customer-facing platforms to back-end systems. This involves not just technological upgrades but also a shift in organizational mindset, prioritizing adaptability and continuous learning to stay ahead of an evolving threat landscape, thereby safeguarding both operational integrity and stakeholder confidence.

Position for Cryptocurrency Growth:

The potential mainstreaming of cryptocurrency, as signaled by JPMorgan, requires a forward-looking strategy that balances opportunity with uncertainty in the financial sector. Rather than waiting for regulatory clarity, institutions should explore experimental initiatives—such as blockchain-based services or digital asset custody—that position them to capitalize on favorable policy shifts while mitigating risks if restrictions tighten.

This approach demands a flexible framework, allowing firms to scale efforts as the market evolves, and emphasizes collaboration with regulators and industry peers to shape emerging standards. The goal is to establish a foothold in this transformative space, leveraging early mover advantages to redefine competitive dynamics without overcommitting to an uncharted domain.

Forge Strategic FinTech Partnerships: The rise of FinTech as a catalyst for innovation, highlighted by Deloitte, necessitates a deliberate approach to collaboration. Leaders should seek partnerships that extend beyond incremental improvements, targeting firms with distinctive capabilities—such as alternative credit assessment or micro-investing platforms—that complement and amplify existing strengths.

This imperative involves a shift from transactional alliances to deep, symbiotic relationships, where shared goals and mutual learning drive long-term value creation. The focus must be on integrating these partnerships into the broader strategic vision, ensuring they enhance agility and market reach while avoiding dilution of core competencies.

The strategic insights and analysis in this report are driven by Nexstrat.ai. Discover how Nexstrat.ai can elevate your strategy development and decision-making—schedule a live demo at nexstrat.ai/book-a-demo.

About NexStrat AI:

NexStrat AI is at the forefront of AI and business strategy innovation. As the ultimate strategy and transformation AI co-pilot and platform, we help leaders and strategists craft winning strategies and make effective decisions with speed and confidence.

Contact Us:

Have questions or want to learn more? Contact us at [email protected]

Follow Us:

Join our community of forward-thinking business leaders on LinkedIn.