Introduction

The GCC AI and Tech sector is rapidly emerging as a global innovation hub, driven by substantial investments, groundbreaking research, and the rapid adoption of advanced digital solutions. In 2021–2024, governments and corporations across the region have bolstered their competitive edge by integrating AI-driven processes, launching local language models, and forming strategic partnerships with global tech leaders. This dynamic environment is fostering an ecosystem where state-of-the-art research meets market application, transforming industries from finance to manufacturing.

Big Moves in Tech Policy and Investment:

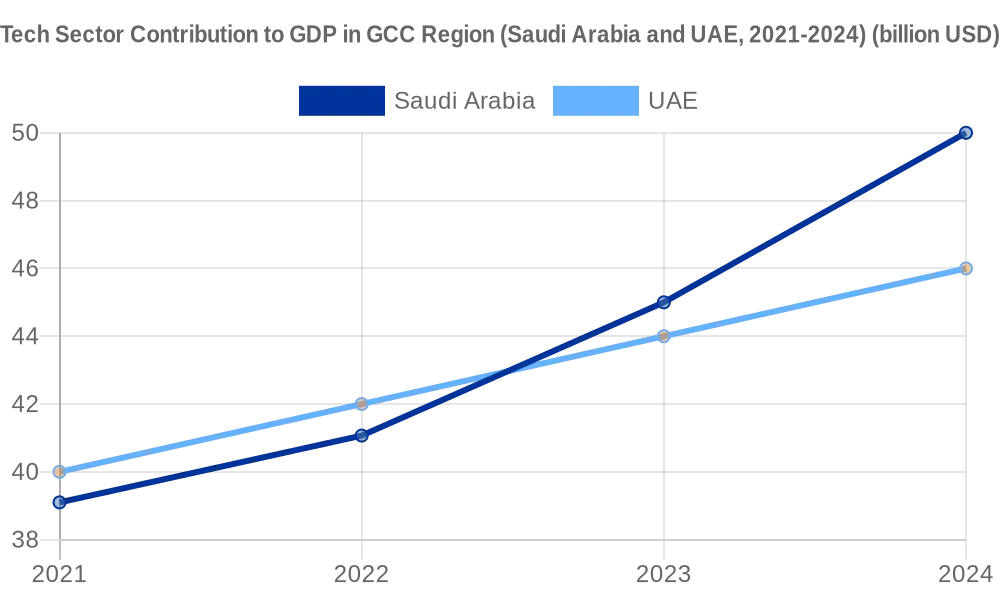

The years 2023–2024 marked a watershed for technology and AI in the GCC, driven by national strategies and hefty investments that position the region as an emerging tech hub. All six GCC countries have elevated tech and AI innovation in their economic agendas. The UAE has been a trailblazer – it launched a National AI Strategy back in 2017 and even appointed the world’s first Minister of AI (pwc.com). Building on that, 2023 saw the UAE unveil ambitious projects like “We the UAE 2031”, aiming to double the digital economy’s contribution to GDP. Saudi Arabia, under its Vision 2030, has poured resources into its own programs via the Saudi Data & AI Authority (SDAIA) and a new initiative called Project “Transcendence” – a $100 billion drive to accelerate AI and advanced tech adoption (middleeastbriefing.com) (middleeastbriefing.com). The Saudi government’s ICT spending grew at a 27% CAGR from 2019–2023, and the 2024 budget allocates $10 billion specifically to digital infrastructure and AI development (middleeastbriefing.com). Clearly, governments are not just talking about tech; they are funding it generously.

Digital Infrastructure Foundations:

One reason the GCC AI and Tech Sector can leap in innovation is the world-class digital infrastructure built recently. The region boasts among the fastest internet speeds globally and extensive 5G networks (Qatar, UAE and Saudi all rank high in 5G coverage). Data center capacity is surging – Saudi Arabia now leads the Middle East with 22 co-location data centers operational and 40 more under development (middleeastbriefing.com), bolstered by investments from cloud giants (e.g. Oracle’s $1.5 billion cloud region, Microsoft’s $2.1 billion investment in Saudi cloud/data centers )middleeastbriefing.com)). The UAE similarly attracted big cloud players: Amazon AWS, Microsoft, and Google all opened UAE cloud zones by 2023. These give local businesses low-latency, secure cloud services to innovate on. Additionally, the GCC’s geographic advantage as a crossroads is being utilized – many undersea internet cables land in the Gulf, and countries are setting up themselves as regional data hubs (Oman is leveraging its multiple submarine cable landings, for instance). This robust ICT backbone – “some of the best in the world,” as PwC notes (pwc.com) (pwc.com) – means the region can support data-heavy AI applications and attract tech companies that need reliable infrastructure.

AI and Emerging Tech Initiatives:

The global explosion of Generative AI in late 2022/2023 (think ChatGPT) found especially enthusiastic adopters in GCC leadership and business circles. By 2023, C-suite interest in AI was sky-high – 73% of Middle East CEOs said they’re keen to embrace new tech like GenAI to transform their businesses (pwc.com). Governments forged high-profile partnerships: In October 2023, the UAE’s leading AI company G42 and U.S.-based OpenAI announced a strategic partnership to deploy advanced AI solutions in the region (pwc.com). Then in April 2024, Microsoft committed a $1.5 billion investment into G42 to collaborate on AI development and to offer G42’s AI services on Azure (pwc.com). This is a landmark deal – one of the largest AI-focused foreign investments in the Middle East – and highlights the global tech community’s recognition of the GCC as an emerging AI player. Saudi Arabia likewise made waves by reportedly buying thousands of high-end NVIDIA GPUs in 2023 to build its own AI supercomputers, and it partnered with China’s SenseTime to develop Arabic-language AI models. Indeed, Saudi Arabia now has 10 supercomputers, 8 of which rank in the global top 500 (middleeastbriefing.com) (middleeastbriefing.com), underscoring its commitment to AI research capacity.

Capabilities in GCC AI and Tech Sector:

Both UAE and Saudi launched their own large language models (LLMs) in 2023–24 – the UAE’s “Jais” model (a 13-billion parameter bilingual model) developed by G42 and Mohamed bin Zayed University of AI, and Saudi’s “Sukkar” (via the Saudi Company for AI) – aiming to tailor generative AI to Arabic and local contexts. These efforts are supported by new research institutions (Qatar opened the Qatar Centre for Artificial Intelligence, UAE has MBZ University of AI, KSA has an Advanced Technology Research Hub under KAUST) (pwc.com) (pwc.com). AI is also being woven into public services: Dubai’s government set a target to automate 100% of government services, and Saudi’s NEOM city promises AI-driven services in safety, logistics, and more from day one. Outside of AI, other emerging tech like blockchain, fintech, and smart cities remain focus areas. Dubai, for instance, has a Dubai Metaverse Strategy (targeting 40,000 jobs in that space) and hosts numerous blockchain conferences. Bahrain and UAE lead in crypto asset regulation, inviting blockchain startups. Meanwhile, Saudi and UAE are competing to be regional centers for electric vehicles and smart mobility – e.g. Saudi’s PIF invested in Lucid Motors (setting up a factory in Jeddah) and launched its own EV brand “Ceer”.

Corporate Adaptation in the GCC AI and Tech Sector– Big Companies Jumping In:

Telecom & Tech Giants:

Regional telecom operators have transformed into tech conglomerates to drive the digital agenda. UAE’s Etisalat rebranded to “e&” and invested heavily in AI, cloud, and fintech (acquiring a majority stake in Careem’s Super App for $400 million in 2023, and a stake in Vodafone plc) to expand digital service offerings. Saudi’s STC formed a dedicated STC Digital unit and an AI subsidiary, and in 2023 STC even launched a $1 billion fund to invest in tech startups globally. These companies are not just improving connectivity; they are becoming content, cloud and fintech players.

Sovereign Wealth Funds:

SWFs like Mubadala and PIF are at the forefront of tech investing. Mubadala’s tech investments span from U.S. tech funds (like the Softbank Vision Fund, which had Saudi/UAE backing) to directly funding local startups and scale-ups. Notably, Mubadala and G42 launched a $10 billion fund targeting tech investments including AI and biotech (mckinsey.com) (iiss.org). PIF established “Savy Games” with $38 billion to develop gaming and e-sports (a form of tech entertainment) and acquired stakes in global gaming companies and local game studios, aiming to make Saudi a gaming hub. PIF’s new strategy also envisions investing $140 billion in AI by 2030 through various subsidiaries (iiss.org).

Private Sector and Startups:

A wave of Gulf startups has risen, many now scaling regionally. Examples: Dubai-based Careem (ride-hailing) was acquired by Uber but its spin-off Super App is now growing in fintech and deliveries with new investment; Saudi’s Jahez (online food delivery) went public in 2022 and is expanding to UAE; Bahrain’s Rain (crypto exchange) is expanding across GCC after meeting local regs. The startup funding environment cooled globally in 2023, but GCC governments partially offset that by injecting capital through venture funds and accelerators (e.g. Saudi’s STV, UAE’s DisruptAD). Corporate incumbents often collaborate with or acquire these startups to inject innovation into their business. Banks partnering with fintechs for digital wallets, retail groups working with e-commerce startups, oil companies funding energy tech startups (Aramco has a $500 million fund “Prosperity7” for frontier tech).

Adoption in Traditional Sectors:

Leading corporations in non-tech sectors are also embracing AI/tech. Aramco uses advanced analytics and AI for predictive maintenance of its facilities, and is piloting blockchain for trading documentation. Emirates Airline and Qatar Airways use AI for route optimization and customer service chatbots. Retailers like Majid Al Futtaim deploy AI for inventory management and personalized marketing. Governments themselves are big adopters: Dubai’s police use AI cameras and predictive algorithms for safety, and Saudi Arabia is implementing e-government and digital justice systems at scale. These use cases not only improve efficiency but also create reference projects that local tech firms can build on.

Risks in GCC AI and Tech Sector:

Hype vs. Reality:

The rush into AI carries the risk of inflated expectations. There is a gap between piloting AI and achieving ROI at scale. Some organizations may invest in trendy tech (like metaverse or blockchain projects) without a clear business case, leading to wasted resources. Ensuring these technologies actually solve problems or create revenue is a challenge – otherwise, there could be disillusionment if promised benefits don’t materialize by 2025.

Talent Shortage:

Perhaps the most acute risk is the shortage of skilled tech talent in the region. While the GCC has no shortage of capital or ambition, human capital is a constraint. There is fierce competition globally for AI researchers, data scientists, and software engineers. GCC firms often have to rely on expatriates, but visa processes and competition from Silicon Valley/Europe for the same talent can hamper hiring. Moreover, national workforce localization requirements mean companies must train citizens in these cutting-edge fields, which takes time. If talent isn’t sufficiently developed, big investments might under-deliver.

Data and Privacy Regulation:

As data becomes the new oil, GCC states are only beginning to formulate data protection and AI ethics regulations. The UAE introduced a Data Protection Law (2021) and Saudi has a draft Personal Data Law – companies will need to comply or risk penalties and public trust issues. Handling consumer data responsibly is critical, especially with open banking and digital government services launching (cyber breaches or misuse of data could erode confidence and draw regulatory backlash).

Cybersecurity and Tech Dependence:

Increased digitization means higher exposure to cyber threats. State-sponsored hacking, ransomware attacks, and AI system vulnerabilities pose significant risks. A major cyber incident could disrupt business or critical infrastructure (imagine a successful attack on a national payment network or on smart city systems). This necessitates robust security measures, which if neglected, could lead to crises. Also, the GCC’s tech ambitions increasingly rely on foreign technology (chips, software) – geopolitical issues (like U.S.-China tech tensions or export controls on AI chips) could impact supply of critical tech components to the region, a risk mostly outside the control of local businesses but important to monitor.

Cultural and Change Management:

Internally, companies face the risk that employees might resist automation or AI deployment, fearing job loss or change. Without strong change management, even great tech initiatives can fail to be adopted, wasting investment.

Opportunities in GCC AI and Tech Sector:

Global Tech Hub Potential:

The GCC is positioning itself as the “third hub” for AI after the US and China (pwc.com) (pwc.com). With the right moves, cities like Dubai, Abu Dhabi or Riyadh could attract international tech companies and talent, becoming the Silicon Valley of the Middle East. We see early signs: multinational tech firms (Amazon, Microsoft, Google) have significant operations; startups from around the world join accelerators in the UAE and Saudi (e.g. Flat6Labs, Hub71). If GCC nations continue to offer incentives (zero tax, grants, visas) and success stories mount, a virtuous cycle of tech clustering can occur.

Homegrown Tech Solutions:

There are unique local needs that GCC AI and Tech Sector can solve and then export. For example, Arabic-language AI applications (for education, media, customer service) are underdeveloped – GCC initiatives in this space can lead to products for 400 million Arabic speakers globally. Likewise, fintech solutions tailored to Islamic finance or migrant worker remittances can be scaled beyond the region. In smart cities, the massive greenfield projects (like NEOM) allow testing of autonomous vehicles, drone deliveries, and IoT at scale in ways most countries can’t – successful models can be commercialized and exported.

Cross-Sector Disruption:

GCC AI and Tech sector is an enabler for others – presenting opportunities for collaboration. For instance, GCC energy firms investing in clean tech startups (like AI for optimizing solar panels, or new battery tech) can spearhead climate tech breakthroughs. Healthcare is another area – Saudi and UAE are investing in digital health (telemedicine, AI diagnostics), which can improve healthcare outcomes and spawn new businesses. The intersection of AI with logistics (e.g. port automation, AI routing for airlines) is also ripe for improvement given the region’s logistics push. Business leaders can find tech-driven efficiency gains in almost every sector, boosting productivity in an era when labor costs (for nationals) are rising.

Venture Capital and Private Equity Growth:

As more tech successes happen, we’ll see growth in local venture capital. The number of GCC-based VC funds is growing, and global VCs are opening offices to scout deals (e.g. in 2023, Sequoia Capital actively looked at GCC startups). This means more funding available for innovative ideas – an opportunity for corporates to perhaps set up CVC (corporate venture capital) arms to invest alongside and keep a pulse on disruptive innovations.

Education and Upskilling Industry:

With the big focus on tech, the education and training sector has an opportunity to boom. Coding bootcamps, AI certifications, and partnerships with global universities to set up campuses (like MIT or Stanford collaborations) can flourish, backed by government support. Businesses can shape curricula by working with these institutions to ensure skills meet market needs. A well-trained workforce will sustain the tech ecosystem’s growth.

Strategic Imperatives for Tech and AI Leaders:

- Bridge the Talent Gap: Invest aggressively in talent development to mitigate the acute skills shortage. This is arguably the single most important imperative. Companies should set up in-house academies or scholarships to train nationals in data science, software engineering, and cybersecurity. Partner with local universities (or even create corporate training institutes) to produce job-ready graduates. In the short term, recruit globally – use the new visa regimes (UAE Golden Visa for professionals, Saudi’s premium residency) to attract top AI researchers and engineers to relocate (pwc.com) (pwc.com). To retain them, create an R&D-friendly culture (freedom to publish, attend conferences, etc.). By building a strong talent pipeline and team, you ensure that tech initiatives have the human power to succeed.

- Embed AI and Tech in Core Strategy: Don’t pursue tech for tech’s sake; tie it directly to business value. Identify key areas where AI/automation can drive competitive advantage – e.g. predictive maintenance in oil & gas, personalized recommendations in e-commerce, or AI-driven risk modeling in finance – and pilot solutions there. The majority of Middle East CEOs already see that GenAI will change how they deliver value (pwc.com) (pwc.com), so boards should ask: Where can tech make us markedly better or more efficient? Set up cross-functional teams (IT plus business units) to implement high-impact use cases first, rather than a scattershot approach. Measure outcomes (cost saved, revenue gained, customer satisfaction upticks) to build the business case for wider rollouts. Essentially, make AI and digital transformation a board-level agenda item with clear ROI targets, ensuring it’s woven into the company’s medium-term strategic plan.

- Forge Strategic Partnerships: Given the fast pace of innovation, leverage partnerships to stay at the cutting edge. Collaborate with global tech leaders through joint ventures or investment deals – as seen with Microsoft’s alliance with G42 (pwc.com). Such partnerships can provide access to the latest tech (e.g. OpenAI models, advanced cloud tools) and knowledge transfer to your teams. Also partner with local tech champions and startups: they often have the agility and creativity to solve problems in new ways. For example, a logistics firm might partner with a drone delivery startup to develop last-mile solutions. Sovereign entities are also open to partnerships – tapping into government-backed innovation programs can bring subsidies and pilot opportunities (e.g. participating in a NEOM smart city pilot as a private vendor). By building a robust ecosystem of partners – universities, startups, global firms, government labs – your company can innovate faster and share risks and rewards.

- Focus on Data and Security Governance: As data fuels AI, ensure you have a strong data strategy and governance framework. Break down silos within your organization so that valuable operational data can be aggregated and used for analytics (respecting privacy rules). Clean, well-structured data is a strategic asset – invest in data platforms and maybe even monetize certain data (some GCC telcos have started anonymized data analytics services, for example). Parallel to leveraging data, double down on cybersecurity. Incorporate security by design in all digital projects. Conduct regular audits and hire ethical hackers to test your defenses. With rising geopolitical cyber threats, consider collaborations with national cyber centers (like Qatar’s NCC, UAE’s Cyber Security Council) to share threat info. Business continuity plans should include responses to cyber-attacks or major IT outages. In sum, treat data as both treasure and something to be zealously protected – a balanced mindset of maximizing value while minimizing risk.

- Champion Innovation Culture and Agility: The success of tech initiatives often boils down to culture. Encourage a culture of continuous learning and innovation in your company. Provide staff with platforms to experiment – hackathons, innovation labs, incubators for internal ideas – and don’t punish failure that comes with prudent experimentation. Flatten hierarchies to speed up decision-making; tech moves fast and your org needs to as well. Also, stay agile by keeping an eye on tech trends and being ready to pivot. For instance, if a new AI technique or a new regulatory framework emerges, have a small team analyze its relevance to your business immediately. Being a first mover (or fast follower) in applying new tech can yield outsized gains. At the board level, consider adding tech-savvy members or forming a technology advisory committee to keep leadership educated and forward-looking. In summary, make adaptability and innovation part of the company’s DNA, so it can ride the tech wave rather than be swamped by it.

Explore more insights on Nexstrat.ai.

About NexStrat AI:

NexStrat AI is at the forefront of AI and business strategy innovation. As the ultimate strategy and transformation AI co-pilot and platform, we help leaders and strategists craft winning strategies and make effective decisions with speed and confidence.

Contact Us:

Have questions or want to learn more? Contact us at [email protected]

Follow Us:

Join our community of forward-thinking business leaders on LinkedIn.