The assessment, analysis, and strategic imperatives in this report are powered by Nexstrat.ai. To experience live how Nexstrat.ai empowers your business in strategy development and decisions, book a demo at nexstrat.ai/book-a-demo.

Introduction

The GCC financial landscape is undergoing a profound transformation. In 2023–2024, regional banks and financial institutions have been retooling themselves to navigate a rapidly changing regulatory environment, increasing digital adoption, and a surge in fintech innovation. Amid tightening global monetary conditions and domestic fiscal reforms, GCC banks are now strengthening their balance sheets and modernizing their operations to remain competitive. The introduction of new taxes, open banking frameworks, and digital finance regulations has paved the way for enhanced transparency and innovation across the sector.

Traditional banking operations are increasingly complemented by digital channels as legacy institutions partner with, or even acquire, fintech startups. This digital pivot is not only reshaping customer experiences—through AI-driven services, enhanced mobile platforms, and seamless payment solutions—but is also redefining risk management and capital allocation. Meanwhile, sovereign wealth funds and government-led initiatives continue to drive investment in fintech, propelling a robust venture capital ecosystem that is transforming the region’s financial services.

In this dynamic setting, financial leaders are tasked with balancing regulatory compliance, risk management, and customer-centric innovation. They must also seize opportunities in emerging markets like SME finance, sustainable finance, and digital wealth management. As the GCC financial sector transitions from traditional banking models to integrated, technology-driven financial ecosystems, a clear strategy that leverages digital transformation, rigorous risk controls, and strategic partnerships becomes critical for long‑term success.

Policy and Regulatory Tailwinds:

The GCC financial sector in 2023–24 has been buoyed by supportive domestic conditions and significant regulatory reforms.

Banking and Fiscal Policy:

High oil prices delivered fiscal surpluses, enabling governments to keep liquidity flowing. While U.S. interest rate hikes (mirrored in GCC pegs) created a monetary tightening, Gulf central banks intervened to ease any strains. In Saudi Arabia, for example, surging credit demand led to the Saudi Interbank Rate hitting record highs, prompting SAMA to inject liquidity (SAR 50 billion in June 2022, and more later) to stabilize markets (pwc.com). By 2023, the “liquidity squeeze” had eased and banks’ lending continued growing, though deposit growth lagged. Crucially, the UAE and others have also deployed counter-cyclical spending to support non-oil sectors, sustaining credit demand.

Tax and Transparency Reforms:

A historic shift is the region’s abandonment of its tax-haven legacy. Following Saudi’s VAT tripling (to 15% in 2020) and Oman/Bahrain introducing VAT, the UAE implemented its first-ever federal corporate tax (9%) in 2023 (reuters.com). Free-zone firms remain exempt on qualifying activities to retain investment appeal (reuters.com) but overall this broadens the tax base. These tax reforms, partly to align with OECD global minimum tax rules, herald a new era of corporate transparency and compliance across GCC financial sector (reuters.com).

Tax and Transparency Reforms:

Regulators in the GCC financial sector have been upgrading capital markets to attract investment. Saudi Arabia’s Capital Market Authority relaxed foreign ownership limits and encouraged a pipeline of IPOs (Saudi saw over 30 listings in 2022–23 on Tadawul and its SME market Nomu). The UAE merged its Securities and Commodities Authority under the central bank for a more unified oversight, and Dubai launched plans to list 10 state companies (e.g. utilities, toll operator) to deepen its market. Meanwhile, Qatar established a new Financial Stability and Innovation Authority in 2023 to spur fintech and market development.

Fintech and Digital Regulations:

Perhaps the most dynamic changes in the GCC financial sector are in fintech regulation. All GCC states rolled out open banking frameworks or guidelines in the past two years, aiming to securely share bank data with fintech innovators (arabianbusiness.com). Bahrain was first with open banking rules, and Saudi followed with its Open Banking Policy in late 2022 (implementation through 2023). In the UAE, regulators addressed previously grey areas – in 2023 the central bank issued rules to license and oversee Buy-Now-Pay-Later (BNPL) providers, bringing fintech credit under supervision (whitecase.com). The Dubai Financial Authority and Abu Dhabi’s FSRA (ADGM) have also introduced robust virtual asset regulations via the Virtual Assets Regulatory Authority (VARA) to govern crypto exchanges. These targeted laws – from BNPL capital requirements in KSA to new crowdfunding and digital payments regulations – signal that authorities are embracing innovation while safeguarding stability (whitecase.com). Overall, the policy environment is pro-growth and reformist: aligning financial systems with global standards (tax, compliance) and encouraging new sectors (fintech, sustainable finance). This gives businesses a more sophisticated and secure financial infrastructure to operate in.

Investment and Market Trends: Bank Performance:

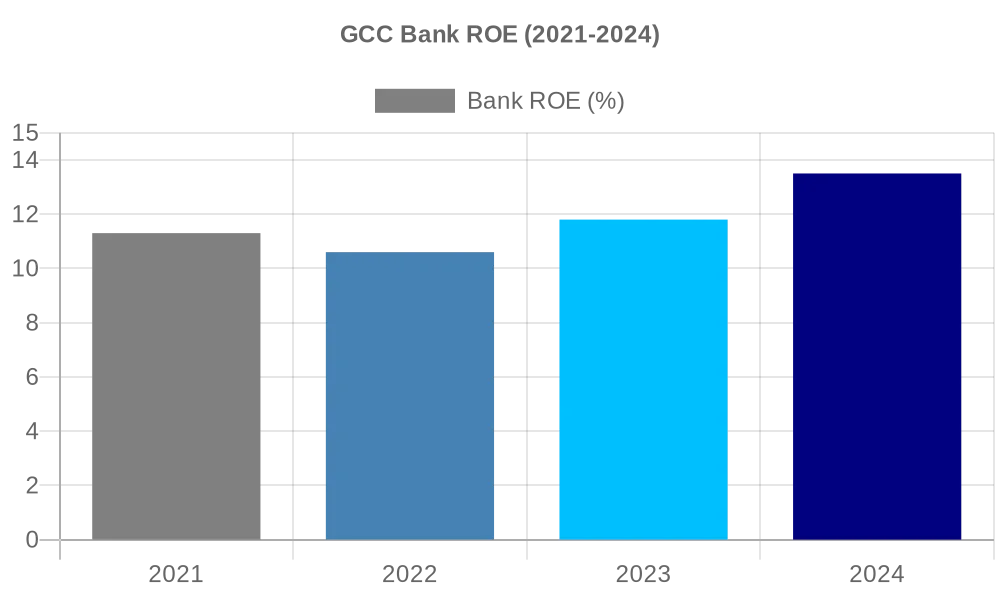

GCC banks entered 2023 in a position of strength, coming off record profits in 2022. In 2023, higher interest rates actually boosted bank net interest margins significantly (most loans re-priced higher, while low-cost deposit bases provided cheap funding). The aggregate return on equity for GCC banks climbed back to pre-pandemic levels (~13–15%) (meed.com). However, loan growth began to moderate late 2023 as borrowing costs rose and some corporates tapped bond markets instead. Saudi banks in particular saw loan-to-deposit ratios stretch above 100%, prompting them to issue more bonds and sukuk to diversify funding (pwc.com).

Capital Markets & Funding:

The GCC financial sector bucked global IPO trends with a vibrant equity issuance pipeline. IPO capital raising in 2023 (notably in energy and tech-related firms) was strong – Abu Dhabi’s ADNOC Gas IPO raised ~$2.5 billion in Q1 2023, Dubai listed several government-related entities (empowering its market capitalization), and Riyadh saw listings ranging from healthcare to financial services. By Q3 2024, financial analysts noted the GCC IPO pipeline remains “healthy… from a diverse range of sectors” (arabnews.com), reflecting sustained investor appetite. Sovereign wealth funds (SWFs) have also been active: while PIF and others continue high-profile global deals, they are increasingly investing at home – e.g. funding fintech startups, infrastructure, and setting up sector-specific funds (Saudi’s Sanabil, ADQ’s tech fund, etc.).

Fintech Boom:

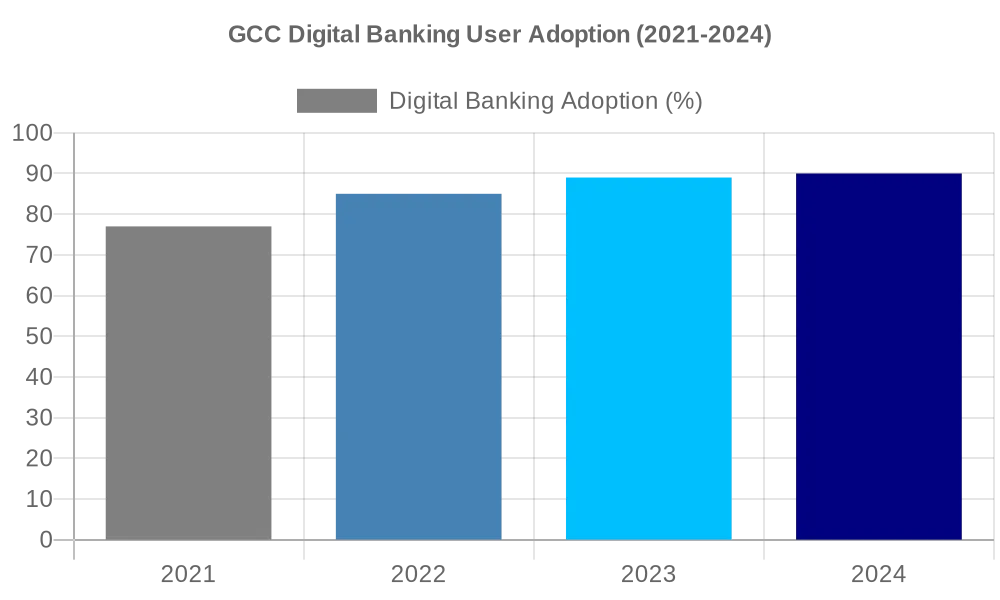

The region’s fintech ecosystem has truly taken off. Between 2017 and 2022, the number of fintech start-ups in MENA multiplied, and 2023 saw heavyweight funding rounds. In Saudi Arabia alone, AI and tech startups raised over $1.7 billion in 2023 (middleeastbriefing.com), a portion of which was fintech (e.g. digital banks, payment processors). Consumer adoption of digital finance is accelerating: usage of mobile wallets, like STC Pay and Dubai’s Payit, is growing rapidly; BNPL services (Tamara, Tabby) became mainstream for retail shoppers (whitecase.com). Additionally, crypto and blockchain have gained a foothold – Bahrain and the UAE host licensed exchanges (Rain, BitOasis), and global crypto players (Binance, Crypto.com) set up regional HQs under new regulations (whitecase.com). Established banks are responding by launching their own digital apps and neo-banks, or partnering with fintechs (e.g. Riyad Bank partnered with Fintech Saudi’s incubator; Emirates NBD’s digital bank LIV targeting millennials).

Sustainable Finance:

Another trend is the rise of green finance. Several GCC banks and corporates issued green and sustainability-linked bonds in 2023 (e.g. Saudi National Bank’s $750 million green sukuk). Abu Dhabi opened a dedicated Sustainable Finance Hub and Saudi’s stock exchange introduced ESG disclosure guidelines. These efforts align with national climate goals and aim to attract ESG-minded global investors.

Insurance and Asset Management:

The insurance sector is consolidating (e.g. mergers in Saudi and UAE) under new solvency regulations, and we see increased penetration due to mandatory health insurance expansions. Asset management is growing too – Saudi’s Public Investment Fund seeded domestic funds and Qatar is encouraging QFC-based asset managers, boosting local capital markets.

How Leading Institutions Are Adapting: Digital Transformation:

Virtually every major GCC bank has a digital transformation program in motion. They are deploying AI and analytics to improve customer service and risk management. For instance, Emirates NBD uses AI chatbots for basic inquiries, and several Saudi banks use blockchain for trade finance. The use of AI in banking is expected to surge; indeed, 73% of Middle East CEOs (across industries) say they are keen to embrace new tech like generative AI, and nearly half have adjusted strategy accordingly (pwc.com). This means bank CEOs are actively budgeting for AI investments, fintech partnerships, core banking system upgrades, and talent in data science.

Geographic and Sector Expansion:

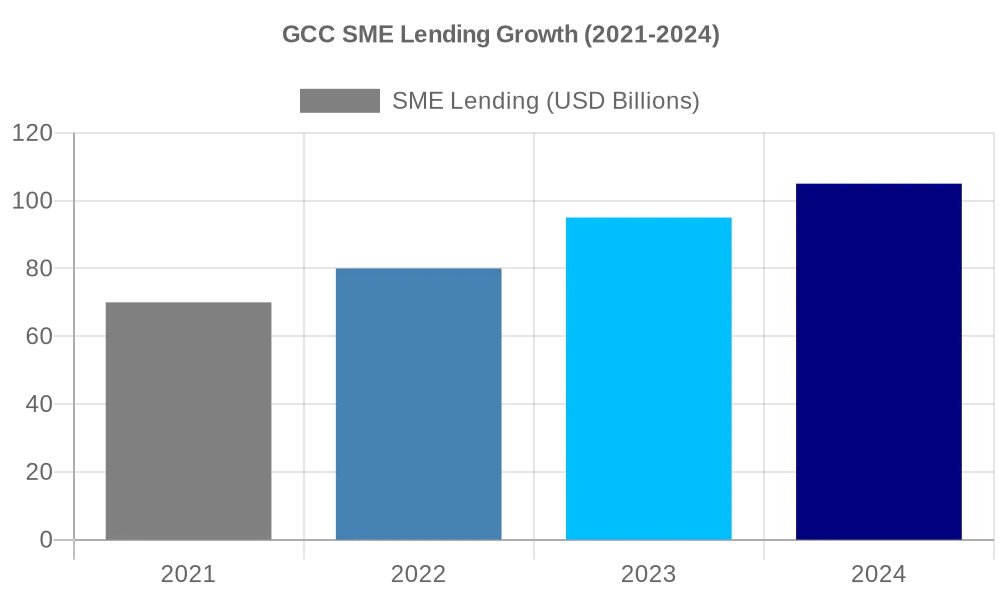

Leading banks are also expanding regionally. First Abu Dhabi Bank (FAB) and Emirates NBD have increased their presence in Saudi Arabia to tap its growth, while Saudi banks like Al Rajhi are opening offices in Gulf neighbors (Kuwait, UAE). Qatar’s big banks (QNB, QIB) continue to diversify abroad (QNB has a major presence in Egypt and Turkey). In terms of sectors, lenders are growing their SME and consumer finance portfolios as these were historically under-penetrated. Governments are nudging banks to lend more to startups and SMEs (e.g. KSA’s Kafalah program guarantees).

Risk & Compliance Upgrades:

With new regulations, banks are beefing up compliance teams – implementing FATF standards to get off grey lists (as UAE did in 2023), preparing for global tax reporting, and meeting Emiratization/Saudization in management ranks. The war for local talent extends to finance: Saudi banks in 2022 had to ensure 90%+ of certain roles are Saudi nationals (pwc.com), so they are heavily investing in training programs to both comply and maintain service quality.

New Entrants and Competition:

The incumbents face fresh competition from digital-only players. Saudi Arabia granted its first digital banking licenses in 2022 (STC Bank and Saudi Digital Bank), which launched operations in 2023 to compete in retail banking via app-only services. In the UAE, digital bank “Wio” (backed by ADQ and Alpha Bank) launched, and independent fintechs offer alternative lending and investment platforms (e.g. Sarwa for robo-advisory, Baraka for stock trading). Even telecom operators are encroaching (e.g. Kuwait’s Zain launched Zain Bank as a digital service). In response, big banks often choose to invest in or partner with these newcomers – for example, Riyad Bank took a stake in digital insurer Tawuniya, and Gulf International Bank launched “Meem,” a digital Islamic bank.

Sovereign Funds and Government Initiatives:

SWFs like PIF, Mubadala, ADIA are not only investors but also market shapers. PIF created the “Saudi Investment Recycling Co.” and other vehicles to develop new sectors (directly affecting project finance). Mubadala’s venture arm is actively co-investing in fintech startups, and ADQ in Abu Dhabi created a fintech incubator Hub71. These moves blur the line between public and private finance but bring huge capital to nascent industries, prompting private players to co-invest or align strategies with government priorities (e.g. focusing on sectors highlighted in Vision 2030).

Risks in the GCC Financial Sector:

Macroeconomic and Credit Risks:

One looming risk is the potential for an asset quality downturn if global or local conditions sour. Thus far, GCC banks have enjoyed low non-performing loan (NPL) ratios (helped by government support during COVID and strong recovery after). But higher interest rates increase debt service burdens – for example, mortgage borrowers in the UAE and Qatar faced steep rate hikes; in Qatar, mortgage uptake actually paused in mid-2024 as consumers awaited rate relief (agbi.com). Should rates remain high or economic growth slow, we could see a rise in defaults, especially in riskier segments like unsecured personal loans or SME credit.

Real Estate Exposure:

GCC banks are heavily exposed to real estate (20–30% of loan books in some cases). With property prices surging, there’s growing concern about a price correction. S&P has warned that “the risk of a cyclical price reversal has increased in Dubai” after two years of rapid gains (spglobal.com). If Dubai’s off-plan market cools or if Saudi’s housing boom slows due to affordability limits, banks could face lower collateral values and slower mortgage growth (spglobal.com). Qatar is already seeing oversupply in some residential segments, which could pressure lenders there spglobal.com).

Competition and Margin Squeeze:

The rise of fintech and new banks means competition is intensifying. While incumbents currently enjoy wide margins, over time digital players could cherry-pick profitable fee income areas (payments, remittances) and force fees and charges down. Also, Big Tech (Amazon, Apple, etc.) might expand financial offerings in the region, further squeezing local banks.

Cybersecurity and Fraud:

As banking goes digital, cyber risk escalates. The region saw some high-profile cyber-attacks (e.g. a major Saudi bank’s systems targeted in 2021); continued threats could undermine trust. Banks need to invest heavily in cybersecurity to prevent breaches that could disrupt operations or lead to financial theft.

Regulatory/Compliance Costs:

Adapting to new taxes, accounting standards (IFRS9 impacts on provisions), and stringent AML/CFT regimes can strain smaller banks. There’s a risk that some weaker institutions, especially in smaller GCC states, might struggle with the cost of compliance and need consolidation. Lastly, talent retention is a subtle risk: with localization policies, banks may have to promote or hire nationals rapidly, potentially creating skill gaps if not managed well – balancing this without hurting performance is an ongoing challenge.

Opportunities in GCC Financial Sector:

Untapped Markets:

Despite the region’s wealth, several financial services segments remain under-penetrated. Insurance density is still low in Saudi and the UAE compared to advanced economies – a huge growth area as awareness increases and as life insurance and savings products gain traction with the middle class. SME financing is being actively pushed by governments; banks that develop tailored SME products (and leverage state guarantees) can build a loyal, lucrative client base. Microfinance and fintech solutions can bring the large expatriate labor population into the formal financial system (for example, prepaid cards, low-cost remittance apps – the UAE saw remittances ~$47 billion in 2023 (arabnews.com), much of it via exchange houses that could be disrupted by digital channels).

Green and Islamic Finance Leadership:

GCC nations can leverage their strengths to dominate in Islamic finance and sustainable finance globally. There’s an opportunity to issue more green sukuk and develop Shariah-compliant ESG investment products – satisfying both ethical and religious criteria, which is a niche only a few markets can serve. As the world of finance looks for sustainable assets, GCC banks can finance solar plants, clean water projects, etc., and securitize those into green investments.

Regional Integration:

The drive to make the GCC a single market (e.g. a unified payments system, harmonized regulations) is ongoing. A more integrated financial market (with “passporting” of financial services across countries) would allow banks and insurers to scale beyond home markets easily. The GCC Cross-Border Payment System launched in 2022 linking Saudi and UAE real-time payment switches is an example, projected to expand to all six states. Business leaders can push for and capitalize on these integration efforts – e.g. by offering cross-GCC cash management services to corporates, or by listing on multiple exchanges to tap a broader investor pool.

Privatization and PPPs:

Governments are privatizing assets (airports, utilities, stock exchanges) and launching public-private-partnership projects (especially in infrastructure). This opens up advisory, lending, and underwriting opportunities for banks and investment firms. For instance, the Saudi Water Partnership Company has tendered dozens of PPP desalination and sewage projects – local banks financing these deals get stable, long-term returns.

Wealth Management & Fintech:

Lastly, the influx of affluent expatriates and repatriation of regional wealth (partly due to global uncertainty) means wealth management is booming. Local financial institutions can capture fees by offering private banking, brokerage, and family-office services that were previously handled in London or Zurich. Digitally, there’s also an opportunity in embedded finance – integrating financial services in non-finance platforms (as per Roland Berger, GCC retail and telecom sectors are embedding finance via loyalty apps, etc.), which can open new revenue streams for those who innovate early (mindster.com).

Strategic Imperatives for Financial Sector Leaders:

- Accelerate Digital and Fintech Integration: Embrace the fintech wave as an opportunity, not a threat. Invest in partnerships or in-house solutions for open banking and AI-driven services. For example, collaborate with open banking platforms like Tarabut Gateway to offer customers unified apps for all accountswhitecase.com. Leverage AI to personalize offerings – GCC consumers are digitally savvy, and a superior user experience can win market share. Importantly, modernize IT infrastructure (cloud adoption, API-enabled systems) to increase agility in rolling out new products. CEOs should set clear digital KPIs (e.g. percentage of sales via digital channels) and possibly create separate digital subsidiaries to foster innovation without legacy constraints.

- Enhance Risk Management and Scenario Planning: The next few years could bring interest rate reversals, real estate corrections, or new taxes – preparedness is key. Strengthen credit risk models by incorporating macro stress tests (e.g. if property prices drop 20% in Dubai or if VAT rises in other countries). Diversify loan portfolios to avoid over-concentration (for instance, expand SME lending to balance heavy real estate exposure) (spglobal.com). Also, revisit liquidity management: lengthen funding tenors by issuing bonds/sukuk proactively, given the manageable refinancing outlook (most GCC corporates have stable credit profiles into 2025) (spglobal.com). On operational risk, invest in cybersecurity and fraud prevention – conduct regular penetration tests and educate customers to maintain trust in digital finance. By anticipating risks and beefing up buffers (capital, provisions), financial institutions can remain resilient even if conditions tighten.

- Leverage New Regulatory Regimes: Rather than seeing new regulations as a burden, turn them into an advantage. The new UAE corporate tax, for example, compels better financial discipline – use it as a catalyst to streamline operations and improve cost-efficiency so that post-tax profits remain robust (reuters.com). Likewise, meet ESG disclosure requirements early to attract green-focused investors and possibly command a premium on valuations. Lead in compliance – banks that are first to implement global standards (IFRS9, Basel III, FATF AML rules) can gain a reputation for reliability, which multinational clients value. Moreover, proactive compliance can avoid penalties and position the bank as a preferred partner for international transactions in an era of de-risking.

- Focus on Customer-Centric Innovation: GCC consumers (both retail and corporate) now expect world-class financial services. Boards should prioritize customer experience as a strategic pillar. This could mean expanding 24/7 service through AI chatbots, offering hybrid advisory models (combining robo-advice with human advisers for wealth clients), and introducing innovative products like Shariah-compliant BNPL or dynamic currency wallets for the large expat workforce. The data shows user adoption of alternative finance is rising – e.g. uptake of BNPL by millennials or crypto trading by high-net-worth individuals (whitecase.com). Rather than cede these segments to startups, incumbent firms should innovate in-house or acquire promising fintechs. A practical imperative is to set up sandboxes or innovation labs internally to pilot such ideas quickly within regulatory bounds.

- Talent and Culture Transformation: Financial leaders must align their organizations’ culture with this fast-changing landscape. That means recruiting new skill sets – data scientists, UX designers, fintech product managers – and upskilling existing staff (especially in branches) to handle advisory roles as routine transactions go digital. With localisation quotas rising (e.g. UAE requires 2% more Emiratis each year in firms with 50+ staffp (pwc.com), banks and insurers should launch training academies to rapidly develop local talent in critical areas like risk management and tech (pwc.com). Additionally, foster an agile culture: encourage cross-functional teams (e.g. IT with business with compliance) to accelerate product development cycles. Empower mid-level managers to make quick decisions so the institution can respond to market changes faster than the traditional hierarchy would allow. In summary, make the organization as innovative and dynamic as the fintechs, while retaining the trust and scale advantages of an established player.

Explore more insights in our blogs on NexStrat.AI.

About NexStrat AI:

NexStrat AI is at the forefront of AI and business strategy innovation. As the ultimate strategy and transformation AI co-pilot and platform, we help leaders and strategists craft winning strategies and make effective decisions with speed and confidence.

Contact Us:

Have questions or want to learn more? Contact us at [email protected]

Follow Us:

Join our community of forward-thinking business leaders on LinkedIn.