Introduction

The GCC logistics sector is transforming rapidly as strategic investments in ports, airports, rail connectivity, and logistics zones converge with government-led reforms and digital innovations. This evolution in the gcc logistics sector is not only bolstering the region’s role as a critical global trade hub but also driving efficiency and sustainability across supply chains. With multimodal infrastructure projects accelerating from 2021 through 2024, the sector is poised to unlock significant economic value and resilience amid changing trade dynamics.

Massive Logistics Upgrades and Policy Initiatives:

The GCC region is in the midst of a logistics infrastructure revolution, driven by both government vision and commercial demand to make the Gulf a premier trade hub. With its strategic location connecting East-West trade routes, the GCC has always had geographic advantage – now it’s doubling down with heavy investment and policy reforms.

GCC National Logistics Strategies:

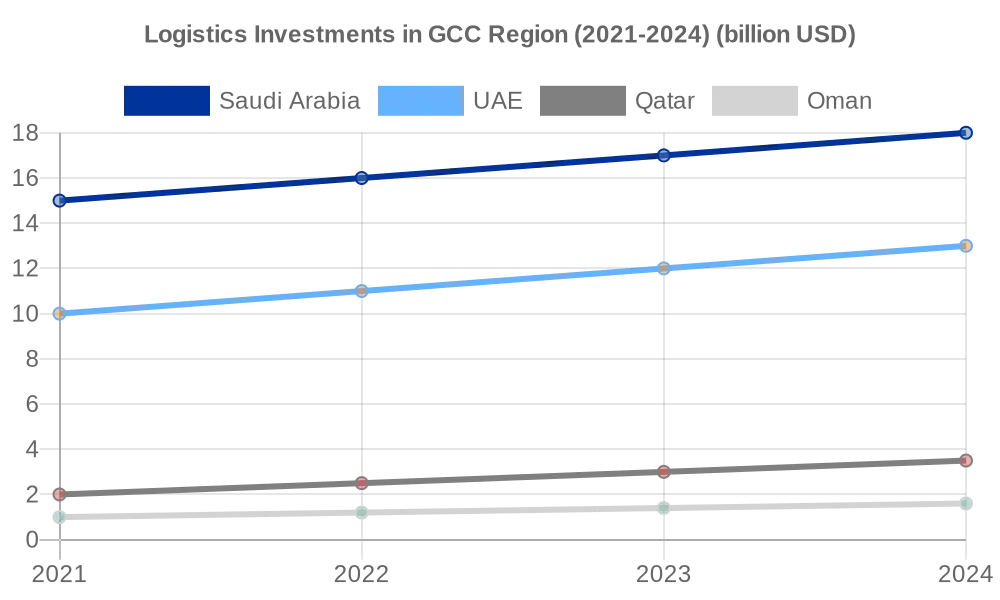

Saudi Arabia launched a National Transport and Logistics Strategy in mid-2021, aiming to position the Kingdom among the world’s top 10 logistics hubs by 2030. This entails increasing port capacities, expanding airports, and developing at least 59 logistics zones (ussaudi.org) (ussaudi.org). In 2023, Saudi officials highlighted progress: customs processes have been overhauled (import clearance times cut from a week to mere hours via the “Fasah” single window platform (ussaudi.org) (ussaudi.org), and dozens of regulations have been updated to streamline licensing and operations in shipping, warehousing and trucking (ussaudi.org) (ussaudi.org.) The UAE, for its part, has a long-established edge with Jebel Ali Port and Dubai as a re-export hub, but it’s not resting – Dubai launched a 2040 Urban Master Plan with significant logistics and port components, and Abu Dhabi is expanding Khalifa Port and its freezone (KEZAD). Smaller states are also active: Oman is marketing its ports (Salalah, Duqm, Sohar) as alternatives that avoid the Strait of Hormuz chokepoint, and investing in road and rail links to GCC neighbors.

Railway Connectivity:

After years of talk, a trans-GCC railway is finally materializing. By 2023, the UAE had completed its national railway (Etihad Rail) linking the major emirates, and in September 2022 UAE and Oman inked a $3 billion partnership to connect via rail (Sohar Port to Abu Dhabi (agbi.com) (agbi.com). Saudi Arabia has its own rail ambitions – the long-discussed Saudi land bridge (linking Red Sea coast to Gulf coast by rail) and connectivity to Jordan and potentially to the UAE via Al Ghwaifat. If these rail links are completed by later this decade, they will revolutionize freight movement, offering faster land routes for goods within the region and beyond.

Aviation Expansion:

Governments are also heavily investing in airports and airlines to boost connectivity. According to Fitch, GCC air traffic could double by 2030 based on current expansion plans (fitchratings.com) (fitchratings.com). Saudi Arabia announced an entirely new airport for Riyadh (King Salman International, to eventually handle 120 million passengers/year) and launched a new flagship carrier Riyadh Air in 2023, ordering 39 Boeing 787s with options for 33 more (iconcox.com). The plan is to turn Riyadh into a major airline hub complementing Jeddah’s focus on religious travel. The UAE’s Dubai World Central (DWC) airport is set for expansion again, and Abu Dhabi opened its long-awaited Midfield Terminal at AUH in late 2023, boosting capacity. Qatar, fresh off a successful World Cup, expanded Hamad International with a stunning indoor garden terminal. Meanwhile, Bahrain upgraded its airport in 2021, and Oman opened a new Muscat airport in 2018 and is now expanding Salalah airport.

Free Trade Zones and Trade Agreements:

Policy-wise, free zones remain central to GCC logistics sector strategy – there’s a proliferation of new special economic zones offering tax and duty exemptions (like Saudi’s integrated logistics zones near airports, and Oman’s freezones by ports). The GCC as a bloc is also negotiating trade agreements (e.g. GCC-UK FTA under discussion, UAE signed CEPAs with India, Indonesia, Turkey in 2022/23) which will increase trade flows. Perhaps most noteworthy, a multinational initiative announced at the G20 in 2023 plans to create a India–Middle East–Europe Economic Corridor, with India-UAE-Saudi rail and sea links to Europe (agbi.com). This grand corridor, if executed, would funnel a huge volume of trade through GCC nodes, firmly integrating the region into global supply chains and elevating its logistics importance.

Infrastructure Investment and Modernization:

Ports:

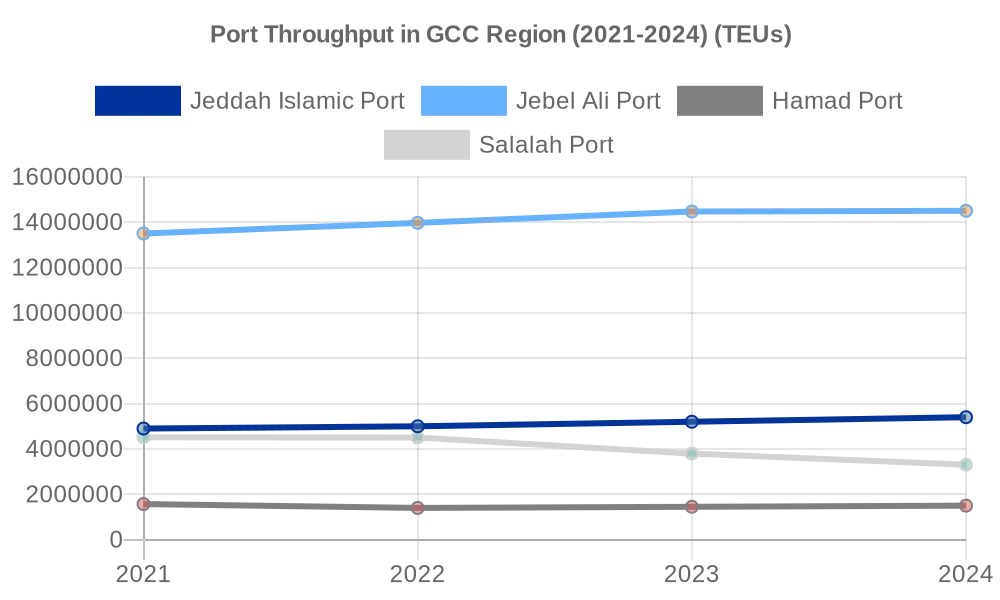

The Gulf’s ports are a lynchpin, handling not only regional import/export but also significant transshipment. Massive upgrades are underway: Saudi Arabia invested SAR 7 billion ($1.9 billion) in 2023 to upgrade Dammam’s King Abdulaziz Port (ussaudi.org) (ussaudi.org), and is expanding Jeddah Islamic Port’s container capacity (in partnership with DP World and others). Seven new shipping services were launched from Saudi ports in early 2023 linking to 43 international ports, including direct routes connecting the kingdom with India, East Africa, and the Mediterranean (ussaudi.org) (ussaudi.org). This diversification of shipping lines reduces dependence on any single route and integrates Saudi more deeply in global networks. The UAE’s Jebel Ali continues to rank among the world’s top ten ports, and Abu Dhabi’s Khalifa Port is adding new terminals (COSCO’s terminal, and another for CMA-CGM) to raise capacity. Oman’s Duqm Port, still in ramp-up, got investments from Gulf and Asian partners to serve as an industrial and transit port (including plans to link to the GCC rail network). Qatar’s Hamad Port (opened 2017) ramped up to handle over 2 million TEU and is positioning as a regional transshipment center with specialized terminals (livestock, coast guard base, etc.).

Integrated Logistics Parks:

Each country is developing logistics parks to capitalize on these port and airport expansions. For example, Saudi’s Logistics Parks around Riyadh and Jeddah, the UAE’s JAFZA and Dubai South (by DWC airport), Bahrain’s Logistics Zone adjunct to Khalifa Bin Salman Port, and Qatar’s new logistics zones near Hamad Port. These parks offer state-of-the-art warehouses, cold storage, and distribution facilities, often with 3PL (third-party logistics) providers on-site. The goal is end-to-end solutions: a company can bring goods through a GCC port, do light manufacturing or assembly in a freezone, then re-export efficiently.

Customs and Process Reforms:

Hardware aside, GCC states have digitized and simplified trade processes significantly. The “Fasah” single-window in Saudi cut clearance times to 2 hours on average in 2022 from 7–12 days a few years prior (ussaudi.org) (ussaudi.org). UAE’s “Dubai Trade” portal similarly integrates all port, customs, and trade financing services online. Gulf countries are also implementing Authorized Economic Operator (AEO) programs (trusted trader schemes) to expedite clearance for accredited companies (ussaudi.org). Also notable is increasing GCC customs cooperation – they are working on a unified transit system so that a truck crossing multiple GCC borders doesn’t face repetitive checks, which will be critical once rail and road connectivity intensifies. These soft infrastructure improvements are as important as the physical expansions in boosting logistics efficiency.

Adaptation by GCC Logistics Companies:

Global and Local Players:

The GCC logistics sector features both global heavyweights and emerging local champions. DP World (Dubai Ports) has evolved from managing Jebel Ali to running a global portfolio of ports – but at home, it’s innovating with automation and expanding Jebel Ali into a multi-modal hub (port + the nearby Al Maktoum airport + logistics zone). Saudi Arabia’s Bahri (the National Shipping Company) historically focused on oil tankers, but it’s expanded into general cargo and even launched its first container shipping line recently, aligning with Saudi’s aim to capture more of its container trade. Major 3PL firms like DHL, Aramex, Agility, and UPS have invested in larger facilities in the Gulf to support e-commerce growth. Aramex (a Dubai-founded company) has restructured to focus on its core express and freight services and is adopting new tech like drones and electric delivery vans for last-mile in Dubai. On the air cargo side, Emirates SkyCargo and Qatar Airways Cargo rank among the world’s top cargo airlines and have been adding freighter aircraft and routes to leverage the surge in e-commerce and time-sensitive shipments. Notably, Riyadh Air is expected to have a dedicated cargo arm, and Saudia Cargo (the incumbent) is expanding, so competition in air freight will heat up too.

Technology Adoption:

The GCC Logistics sector companies are heavily adopting technology to improve visibility and efficiency. Many are implementing AI for route optimization (especially trucking routes to avoid congestion at borders) and warehouse automation (robots sorting parcels in Amazon and Noon fulfillment centers in Dubai/Riyadh). Blockchain pilots are being run for trade finance and documentation (Dubai’s TradeLens blockchain, jointly with Maersk and IBM, has been trialed to digitize Bills of Lading). The use of IoT sensors for cold chain monitoring is rising, critical for vaccine and food imports in the Gulf’s climate.

Strategic Shifts:

Recognizing the need for integrated offerings, freight forwarders and carriers are offering end-to-end solutions in the GCC logistics sector. For example, Maersk set up its own 100k sqm warehouse in Dubai in 2023 to offer integrated ocean+warehouse solutions. Companies are also expanding regionally – e.g. UAE’s Tristar Group (fuel logistics) expanded into Oman and Kuwait. And with new opportunities like the India-Middle East corridor, logistics firms are forming alliances: Indian Railways and DP World might partner on land logistics to connect to Gulf ports, etc.

Startups and New Entrants:

A dynamic development is the emergence of logistics tech startups – e.g. Saudi’s Trukker (an “Uber for trucks” digital platform) has grown across GCC and beyond, providing freight matching services. Last-mile delivery startups like Nana Direct (groceries) or Fetchr (parcels) have seen mixed success, but the trend is clear: the sector is ripe for disruption by tech-enabled models, and incumbents are either acquiring or launching similar apps. For instance, Aramex invested in last-mile startup MyUS to enhance its cross-border e-commerce capabilities.

Risks in GCC Logistics Sector:

Global Trade Fluctuations:

The GCC logistics sector is tied to global trade health. If worldwide trade volumes dip (due to recession or protectionism), Gulf ports and carriers could see slower growth or excess capacity. On the horizon, some uncertainty stems from geopolitics – the war in Ukraine shifted some trade flows (more oil going East, grains needing new routes), and the outcome of conflicts can change demand for Gulf logistics. A positive resolution (as AGBI speculates, an end to conflicts could reopen routes via Syria/Lebanon) (agbi.com) (agbi.com) would benefit Gulf trade via the Levant, whereas escalation in other areas could divert more trade around the Cape of Good Hope (bypassing Suez/Gulf) (agbi.com) (agbi.com).

Regional Competition & Overcapacity:

All GCC countries want to be logistics hubs – but can the region support multiple mega-hubs simultaneously? There’s potential overcapacity if, say, Jeddah, Dubai, and Doha all expand container terminals aggressively beyond what the region and hinterland can fill. Already, some observers note “competition due to continued new retail space” in real estate (spglobal.com) – similarly, too many port or airport expansions could lead to price competition and underutilization. GCC governments will need to balance national pride projects with realistic demand.

Security of Trade Routes:

The Gulf’s trade arteries are generally safe, but incidents like the occasional Houthi attacks on ships in the Red Sea (as seen in past years) or mines in regional waters pose risks (agbi.com) (agbi.com). The Strait of Hormuz is a chokepoint that Iran could threaten in conflict scenarios, which is why Oman’s ports and the UAE’s Fujairah (outside Hormuz) are strategic. The new Red Sea naval alliance and regional diplomacy are aimed at mitigating these threats, but logistics planners always have to have contingencies for route disruptions (e.g. diversions around the Cape of Good Hope which increase transit time (agbi.com)).

Talent and Know-How:

Operating advanced logistics infrastructure requires skilled manpower – port crane operators, supply chain managers, pilots, etc. There’s a talent gap in specialized areas like maritime engineering and railway operations, since some GCC states have never had extensive rail networks before. They’ll rely on international expertise initially, but must develop local human capital to sustain operations.

Environmental Regulations:

Internationally, shipping is facing stricter environmental rules (IMO low-sulfur fuel requirements, future carbon taxes on shipping). GCC ports and ship operators will need to adapt (e.g. providing cleaner fuels like LNG bunkering at ports). Also, an increased environmental consciousness could affect air freight (pressure to reduce carbon footprint might shift some volume from air to sea or sea-rail combos). Gulf logistics providers should stay ahead by adopting green initiatives (like electric port vehicles, green warehouses) to meet the sustainability expectations of global clients.

Opportunities in GCC Logistics Sector:

E-commerce and Last Mile:

The e-commerce market in MENA is expected to exceed $50 billion by mid-decade, and GCC is the biggest chunk. The surge in online shopping (especially post-pandemic) is a boon for warehousing, fulfillment, and last-mile delivery services. Companies can invest in automated fulfillment centers and urban delivery networks. Same-day delivery is becoming a norm in UAE and Saudi cities – expanding these capabilities (using decentralized micro-warehouses closer to customers) is an opportunity in the GCC logistics sector.

Multimodal Logistics and Value-Added Services:

With rail coming, the concept of multimodal transport (seamlessly moving goods from ship to rail to truck) becomes feasible. Firms that can integrate these modes will offer faster, cheaper transport. For instance, a container from India could land in Dubai and go by rail to Dammam, then truck to Kuwait – a seamless service offering that previously would require multiple handovers. Additionally, providing value-added services in free zones (assembly, packaging, labeling) can attract manufacturers to use GCC as a distribution center. A Chinese electronics company, for example, could ship bulk to Dubai, do final kitting and software loading in a freezone, then distribute regionally – capturing that business is an opportunity for those who offer such integrated logistics solutions in the GCC logistics sector.

Regional and South-South Trade:

The GCC logistics sector can capitalize on growing trade lanes, not just East-West but South-South (e.g. between Asia and Africa, using GCC as a stop). Ports like Jeddah and Salalah are well placed for transshipment into East Africa. Already Chinese exporters are trialing “hybrid sea-air” routes that ship goods to Gulf hubs then airlift to Europe, to cut cost and avoid disruptions like Suez closures (agbi.com) (agbi.com). Developing these hybrid logistics solutions can make GCC providers indispensable in global supply chains.

Logistics Tech and Innovation:

The confluence of tech and logistics (LogTech) is a nascent but growing field locally. Autonomous trucks in controlled routes (perhaps within large ports or between certain logistics zones) could reduce costs – trials could happen in the UAE’s empty desert highways or within NEOM’s tech-friendly environment. Drone deliveries in less congested Gulf cities are plausible – Dubai has tested them for medical deliveries. Companies that innovate in these areas could set industry standards.

Humanitarian and Niche Logistics:

The GCC’s strategic spot also allows it to be a hub for humanitarian logistics (Dubai’s International Humanitarian City is already a base for UN relief stockpiles, enabling quick response to crises in Africa or Asia). This not only is good CSR but also brings business in storage and charter flights. Another niche is cold chain (for pharma, perishables) – by building advanced cold storage and certified handling processes, Gulf hubs can capture more of the high-value pharmaceutical transit market between Europe and Asia (Qatar and UAE are eyeing this).

Strategic Imperatives for GCC Logistics Sector Leaders:

- Capitalize on Infrastructure – Fill the Capacity: With billions invested in shiny new ports, airports, and rail, the imperative for operators is to drive volume through these assets. That means aggressively courting shipping lines, airlines, and logistics customers with attractive rates and services. Form alliances: e.g. a port might partner with a major shipping line to make it their regional hub, guaranteeing certain throughput. Similarly, airlines and airports can strike deals (like Emirates and Dubai have symbiotically grown). If you operate a new rail or logistics zone, actively integrate with customers’ supply chains – offer seamless end-to-end solutions (customs clearance, last-mile delivery) so using your facilities is a one-stop proposition. Essentially, focus on customer acquisition to prevent underutilization of capacity. Market the GCC’s stability and efficiency as an alternative to congested or risky nodes elsewhere.

- Streamline and Digitize Operations: Efficiency is a key differentiator in logistics. Leaders should continue streamlining processes via digitalization. Aim for fully paperless trade – build on single-window systems to incorporate blockchain for bills of lading, IoT for real-time tracking of containers, AI for dynamic rerouting of shipments during disruptions. By cutting transit times and increasing reliability, GCC logistics can stand out. For example, Saudi reduced import documents from 12 to 2 (ussaudi.org) – keep pushing such simplifications region-wide. Internally, invest in warehouse automation and port machinery upgrades (e.g. remote-controlled gantry cranes, automated guided vehicles in ports) to increase throughput per hour. A data-driven approach (using analytics on port dwell times, truck turnaround, etc.) can identify bottlenecks to attack. Remember, shippers will choose routes that are faster, cheaper, and predictable – make your operations epitomize those qualities.

- Develop Multimodal Expertise: Think beyond single modes. True logistics powerhouses manage the interplay of sea, air, and land. With rail coming into play, ensure your company or port is ready to offer integrated services. If you’re an airport operator, consider partnerships with shipping companies to feed cargo into your freighters (sea-air). If a port, maybe operate an inland dry port connected by rail to extend your reach. Breaking silos between modes will be key. Customers increasingly want a single contract to move goods door-to-door across modes – provide that. For instance, a logistics firm could offer to take a container from Shanghai factory, move by sea to Jebel Ali, transfer to rail to Riyadh, and truck to final Saudi destination, all under one bill. That’s powerful. It may require acquiring or partnering with companies in other modes (e.g. a port operator partnering with a rail operator). Those who achieve true multimodal integration first will capture market share and loyalty.

- Embrace Sustainability and Resilience: Global clients are pushing logistics providers on carbon footprint. Proactively green your operations: invest in electric or hydrogen port equipment, optimize routes to minimize fuel use, and even explore alternative fuels (like offering LNG bunkering for ships or SAF – sustainable aviation fuel – for airplanes). By doing so, you not only appeal to environmentally conscious customers but also pre-empt future regulations. Also, build resilience – recent years taught the world about supply chain shocks (pandemics, Suez blockage). Develop contingency plans: e.g. maintain some spare capacity to handle sudden surges, diversify sourcing of critical parts for your operations, and coordinate with government on security (so that in crises, you can keep operating). Highlighting a robust business continuity plan can be a selling point to customers choosing a hub for their distribution.

- Invest in People and Partnerships: As with other sectors, the human element is crucial. Train the next generation of logistics professionals. With new tech like cranes and automated systems, ensure your workforce is upskilled. Partner with educational institutes to start courses in supply chain management, port operations, and rail logistics. Having skilled people will maintain service quality. Moreover, don’t shy from public-private partnerships: many logistics improvements (like cross-border trade systems, rail networks) involve government. Engage with policymakers to shape sensible regulations and to coordinate development (e.g. aligning port customs hours with rail schedules). The more the private sector and government collaborate, the smoother the overall logistics ecosystem. This also includes cooperation among GCC countries – push for the full implementation of the GCC Customs Union and unified standards, which will directly benefit your business. A collaborative approach, both internally (with staff) and externally (with governments and even competitors for standards), will help the region achieve the vision of being a top logistics hub.

Explore more insights on Nexstrat.ai.

About NexStrat AI:

NexStrat AI is at the forefront of AI and business strategy innovation. As the ultimate strategy and transformation AI co-pilot and platform, we help leaders and strategists craft winning strategies and make effective decisions with speed and confidence.

Contact Us:

Have questions or want to learn more? Contact us at [email protected]

Follow Us:

Join our community of forward-thinking business leaders on LinkedIn.