Introduction

Over the past few years, the GCC real estate sector has experienced transformative growth, driven by strong demographic trends, strategic government initiatives, and robust foreign investment. From 2021 through 2024, key markets such as Dubai, Riyadh, and Doha have witnessed significant price appreciations in both residential and commercial segments, while urban redevelopment and sustainable building practices are redefining market dynamics. Policy reforms aimed at increasing housing affordability and encouraging smart city initiatives have further enhanced market transparency and investor confidence in the GCC real estate sector. This analysis distills these trends into actionable insights, offering a clear roadmap for navigating the evolving real estate landscape in the region.

GCC Real Estate Sector Overview:

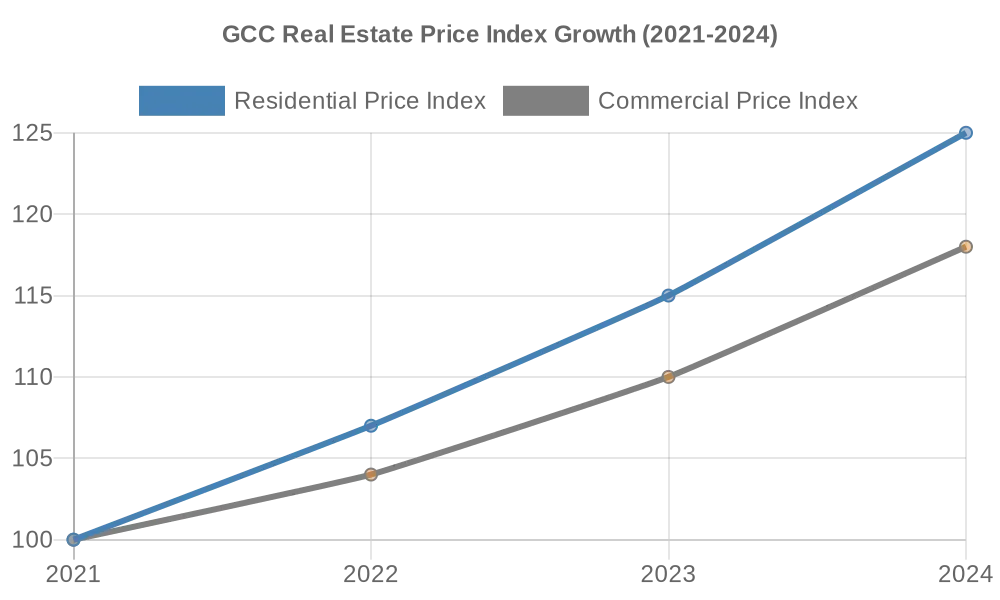

The GCC real estate sector surged through 2023–24 on the back of economic growth, population influx, and mega-project momentum. Across the Gulf, property markets saw record-high transactions and price gains in prime areas, although with some signs of overheating. Total real estate deals across GCC countries reached $383 billion in 2024, up sharply from prior years (arabnews.com) (arabnews.com). The boom was especially evident in the UAE and Saudi Arabia – Dubai alone accounted for $207 billion (54%) of that transaction value, while Saudi’s transactions jumped 47% year-on-year to $75.7 billion in 2024 (arabnews.com) (arabnews.com). Key drivers have been rapid population growth (both natural and via expatriates), government-backed development programs, and a post-pandemic rebound in tourism and business activity. Policymakers have also enacted pro-property measures: Saudi Arabia, for example, is mid-way through an ambitious housing program to raise home ownership to 70% by 2030, offering subsidized mortgages to citizens. The UAE introduced Golden Visas and 100% foreign business ownership, attracting long-term foreign residents who increasingly invest in homes rather than rent (arabnews.com) (arabnews.com). Even Qatar, after the World Cup, has eased rules to lure foreign real estate investors, establishing a new regulatory authority “Aqarat” in 2023 to streamline property ownership for foreigners (agbi.com). In short, the policy stance has been to encourage real estate growth as a means of diversification and urban development – but with that success come new challenges of affordability and sustainability.

Major Trends and Developments in the GCC Real Estate Sector:

Residential Real Estate – Soaring Demand vs. Affordability:

In most GCC cities, residential prices and rents have been rising continuously since 2021. Dubai saw extraordinary activity – 2023 was its best year on record for home sales, with Q3 sales and mortgage volumes at all-time highs (agbi.com). Prices in sought-after villa communities and waterfront properties climbed, in some cases surpassing 2014 peak levels. Average house prices in Dubai rose ~20% in 2023, and Abu Dhabi also registered robust growth in both prices and rents through 2024 (agbi.com) (agbi.com). Saudi Arabia experienced a housing crunch in Riyadh: with Vision 2030 projects drawing expatriates and jobs, “housing became a scarce commodity in 2024”, and residential transactions in the capital rose 31% y/y by Q3 2024, according to CBRE (agbi.com) (agbi.com). This pushed Riyadh apartment and villa prices up ~4–5% in a year(agbi.com.) Government initiatives like the National Housing Company’s large-scale affordable housing communities also sold rapidly, indicating appetite at both the high-end and middle segments (agbi.com). However, this rapid growth is splitting the market: industry observers note a “growing gap between top-quality properties and second-tier ones” (agbi.com). Prime locations and new builds see intense demand and price appreciation, whereas older or less ideally located properties lag. For instance, in Qatar’s 2024 market, Grade A apartments in Lusail or West Bay remained in demand, but secondary locations struggled to maintain occupancy (agbi.com) (agbi.com). Likewise in Oman, demand remained soft – Muscat saw apartment prices fall 13% y/y in Q3 2024 amid high interest rates, with only a slight uptick in villa prices (agbi.com). The key concern now region-wide is affordability. In Saudi, rents jumped 10%+ in 2024 in major cities, outpacing income growth and putting pressure on household budgets (arabnews.com) (arabnews.com). Dubai’s average unit size sold has shrunk to historic lows as buyers opt for smaller, more affordable units (agbi.com) (agbi.com). Housing affordability is a political and economic issue that authorities are watching closely. We may see more measures (e.g. Saudi’s rent cap discussions, UAE affordable housing quotas) if prices continue out of reach for middle-class residents.

Commercial Real Estate – Offices and Retail:

The rebound in business activity led to a revival in office markets, especially in Saudi and the UAE. Grade A office occupancy in Riyadh and Dubai hit near 90–95% in core business districts by late 2023 (agbi.com) (agbi.com). Riyadh’s severe shortage of quality office space drove rents to record highs in 2024 – some reports cite rent increases of 20–30% in prime zones as multinational firms set up regional HQs (spurred by Saudi’s HQ Incentive program) (agbi.com) (agbi.com). Dubai also saw office sale prices jump 15% and rents 25% y/y in prime areas by Q3 2024 (agbi.com) (agbi.com), fueled by new company formations and an influx of family offices relocating to the tax-friendly environment. In contrast, secondary office space and older buildings see weaker demand, and in some markets like Bahrain and Oman office rents remain flat or with high vacancy, reflecting their slower economic pace. Retail real estate presents a mixed picture. The revival of tourism and consumer spending post-COVID led to high footfall in prime malls (e.g. Dubai Mall, Mall of Saudi under construction) and improved tenant sales, enabling landlords to push rents up modestly and fill vacancies(spglobal.com) (agbi.com). The UAE’s top malls report near full occupancy and are integrating more entertainment to keep foot traffic high (spglobal.com). Saudi Arabia’s retail segment similarly benefited from a 27% jump in international visitors (largely religious tourism) in the first 9 months of 2024, boosting malls and shops in Makkah/Madina and central Riyadh (agbi.com) (agbi.com). However, secondary retail centers – older strip malls or shops in less dense areas – are struggling with competition from e-commerce and newer venues(agbi.com.) Throughout the GCC, omnichannel strategies (retailers blending online and offline) are affecting store footprint decisions. Some big retail developers are repurposing spaces, adding warehouses or dark store spaces for online fulfillment within malls.

Hospitality and Specialty Real Estate:

The GCC hospitality sector boomed as well, benefiting real estate tied to tourism. Dubai exceeded pre-pandemic tourism levels, hosting 14+ million visitors in 2022 and more in 2023, which kept hotel occupancy in the 70–75% range with record average daily rates (though rates plateaued in 2024 due to inflation pressure on travelers (spglobal.com)). Saudi Arabia saw a tourism upswing from new entertainment events and easier visas, with international visits up sharply (e.g. Riyadh Season, AlUla events). Hotel developers are rushing to add supply in Riyadh, the Red Sea coast, and religious cities; even so, demand has largely absorbed new openings. Qatar had a unique situation post-World Cup: a huge increase in hotel room supply in 2022 led to a softer market in 2023, but improved tourist arrivals in 2024 helped a recovery (agbi.com) (agbi.com). Notably, Ras Al Khaimah (UAE) embarked on a landmark project – a $3.9 billion Wynn Resorts development featuring the GCC’s first casino, slated by 2026. This has triggered a construction and land price surge in RAK’s hospitality segment as it positions to capture high-end gaming tourism (agbi.com) (agbi.com).

Logistics and Industrial Real Estate:

A segment often overlooked is logistics real estate – warehouses, distribution centers, and industrial parks – which is quietly booming due to e-commerce and manufacturing drives. In 2023, demand for modern warehousing in Dubai and Riyadh outstripped supply, leading to record-high rents for grade A warehouses (e.g. Dubai’s JAFZA industrial rents rose and vacancy hit record lows). Governments are building vast industrial cities (like Egypt’s cooperation on Saudi’s OXAGON at NEOM, or Oman’s Sohar Freezone expansion) that blend manufacturing with logistics, offering opportunities for real estate developers to provide worker housing and commercial facilities in those zones.

Corporate Strategies and Notable Players in the GCC Real Estate Sector – Developers Riding the Wave:

Major real estate developers are capitalizing on strong markets with new project launches and strategic shifts. In the UAE, Emaar Properties, the region’s largest developer, posted robust earnings and resumed launching mega-projects (e.g. “The Oasis” luxury community in Dubai, announced 2023). They and peers like Damac are tapping capital markets for growth – Damac raised $750 million via a sukuk in 2023 to fund projects (agbi.com) (agbi.com). Many UAE developers are also expanding abroad (Emaar in Egypt and India, Aldar in Egypt and through partnerships in KSA) to diversify revenue.

Saudi Giga-Projects:

In KSA, PIF-backed development companies (NEOM Co., Roshn for housing, Red Sea Global for tourism) are essentially creating entirely new cities and resorts. These entities operate like corporate developers with massive budgets, deploying new technologies (e.g. modular construction, smart city tech) at scale. Their strategy often involves partnering with foreign architects and hotel operators to ensure world-class standards. A side effect: they are pushing sustainability norms (NEOM’s projects aim for 100% renewable energy and innovative urban design like “The Line”). Traditional Saudi developers (e.g. Jabal Omar in Makkah, Al Akaria) are adjusting by forming joint ventures with these giga-projects or focusing on niches (like luxury residential in Riyadh’s Diplomatic Quarter).

PropTech Adoption:

There’s a growing trend of real estate firms embracing technology – from using AI for property management to virtual reality for sales. Statements from executives (like Sakan’s CEO in Saudi) highlight that “PropTech is no longer an option; it is a necessity” (arabnews.com) (arabnews.com). We see property listing portals, digital mortgage platforms, and smart-home features becoming common. Some GCC developers are investing in PropTech startups to gain an edge in efficiency (for example, Aldar launched a $100 million PropTech fund in 2023).

REITs and New Financing Models:

To attract more investment, real estate players are using Real Estate Investment Trusts (REITs) and other vehicles. Saudi Arabia now has 18+ listed REITs giving exposure to retail investors. The UAE saw its first REITs and more are in pipeline. These provide liquidity and price discovery to the property market. Also, fractional ownership models and crowdfunding of property (through regulated platforms) have emerged, letting smaller investors partake. Corporate real estate owners (like hotel groups or mall operators) are monetizing assets through such structures to recycle capital for growth.

Sustainability and Standards:

Leading firms are starting to differentiate through sustainability – e.g. Majid Al Futtaim Properties (which runs malls/hotels in UAE & Oman) pledged to be net positive in water and carbon by 2040, installing solar panels on malls etc. While not yet a primary demand driver, there’s anticipation that future regulations will enforce green building codes, so some are getting ahead.

Risks and Challenges in the GCC Real Estate Sector – Overheating and Correction Risk:

After two years of steep climbs, there’s rising concern that certain markets may overheat. Dubai, for instance, has a history of boom-bust cycles; the proliferation of off-plan sales (which made up a majority of transactions in 2023) (agbi.com) has some analysts warning of a potential oversupply “bubble brewing” in that segment (agbi.com) (agbi.com). If investor sentiment changes or if a global recession hits, off-plan buyers might default, leading to project slowdowns. Qatar’s post-World Cup oversupply (especially in residential apartments) is a cautionary tale – oversupply there has led to rent softness in non-prime units (spglobal.com).

High Interest Rates:

Financing costs have roughly doubled since 2021 due to rate hikes. While many GCC home purchases are cash, mortgage uptake is growing (especially among expats in UAE/Saudi). High interest costs can dampen demand or strain recent buyers with floating rates. In Oman, for example, high rates clearly subdued the market in 2024 (agbi.com). The expectation of rate declines in 2024–25 (as inflation is tamed) is a positive, but any delay in that pivot could weigh on affordability longer.

Affordability and Social Risk:

As noted, if locals feel priced out of housing or rents skyrocket, governments may intervene (rent controls, more public housing). Already, Saudi’s home ownership gains are threatened by expensive urban land – Riyadh land prices have soared, pushing affordable housing to city outskirts. GCC leaders won’t want a real estate boom that leaves nationals behind, so firms should brace for possible policies like affordable housing quotas in new developments or stricter rent caps.

Regulatory Changes:

The regulatory environment is generally supportive, but changes can occur. E.g., Dubai periodically adjusts visa or ownership rules which can sway demand. Qatar’s new rules aim to attract investors, but elsewhere one could see cooling measures if needed (such as higher transaction fees for speculative flips – Dubai did this in past cycles). Also, evolving strata laws (joint ownership rules) and digital title systems are being implemented, requiring developers and brokers to adapt to more transparency and professional management of properties.

Construction Costs and Execution:

The construction sector is under pressure from high materials costs and contractor capacity limits. Many GCC projects have faced delays due to contractor overstretch or supply chain delays (e.g. façade materials long lead times). This can delay handovers and cash flows for developers. Additionally, labor reforms (like stricter worker welfare standards) can raise costs but are necessary for sustainability of the sector.

Opportunities in the GCC Real Estate Sector:

Middle-Class and Affordable Housing:

A major opportunity is in the underserved middle-income housing segment. With 800,000+ new housing units needed across Saudi, Kuwait, and Oman by 2030 to meet demand (arabnews.com) (arabnews.com), developers who can efficiently build reasonably priced homes will find a huge market. Governments are supportive – e.g. providing land or financing incentives for affordable projects. Private players can tie up with housing programs (like Saudi’s Sakani) to secure buyers.

Tourism and Hospitality Real Estate:

The GCC’s pivot to tourism (Saudi aims for 100 million annual visits by 2030) means high demand for hotels, resorts, theme parks, and entertainment complexes. Companies can seize this by developing hospitality assets or REITs focused on tourism real estate. Niche markets like eco-tourism (resorts in Oman’s mountains or KSA’s nature reserves) and cultural tourism (heritage sites lodging) are nascent but promising as the region diversifies beyond luxury shopping tourism.

Logistics and Data Centers:

As e-commerce grows (Amazon, Noon) and GCC positions as a logistics hub, modern logistics facilities are in short supply. Developing warehouse parks, last-mile delivery centers near cities, and cold storage facilities can be very lucrative (backed by long leases from logistics firms). Similarly, the digital economy needs data centers – several new data center projects are underway (e.g. Microsoft and Oracle building cloud regions in Qatar and Saudi (middleeastbriefing.com)). Real estate investors can partner with tech firms to build data center real estate (essentially specialized warehouses with power/cooling), a high-growth asset class globally that is now coming to the Gulf.

Redevelopment and Urban Regeneration:

Some GCC cities have aging stock (e.g. older apartment blocks in Dubai, old commercial souks). There’s opportunity in redevelopment – upgrading or replacing old structures with modern mixed-use developments. For example, Dubai’s Deira and parts of Abu Dhabi island have revitalization plans; developers who engage in these public-private urban regeneration projects can unlock value in prime locations.

PropTech and Smart Cities:

The push for smart cities (NEOM, Dubai Silicon Oasis expansion, etc.) means all new projects will incorporate tech – IoT sensors, smart grids, autonomous vehicle infrastructure. Firms that build expertise in smart buildings can differentiate their projects and possibly charge a premium. Additionally, investing in PropTech (online brokerage, 3D printed construction, AI property management) can reduce costs and appeal to a new generation of buyers and tenants.

Strategic Imperatives for Leaders in the GCC Real Estate Sector:

- Diversify Offerings to Address Gaps: It’s time to rebalance portfolios. Don’t just chase luxury; also tap the underserved mid-market. For developers, this means designing smaller, more affordable units and using value engineering to lower costs per unit. The data shows huge demand for reasonably priced housing – e.g. 800k new units needed by 2030 in key markets (arabnews.com). By partnering with housing programs or offering rent-to-own schemes, companies can capture this volume segment and enjoy stable sales, even if high-end demand cools. Similarly, commercial developers should consider emerging asset classes like logistics parks or healthcare facilities, diversifying beyond pure office/retail.

- Be Cautious and Data-Driven in Expansion: Given potential overheating, use data analytics to guide investment decisions. Closely monitor supply pipelines and demand signals. For instance, track the ratio of off-plan sales to end-user mortgages – if speculative activity seems too high, adjust and focus on ready or near-completion projects to mitigate risk (agbi.com). Companies should stress-test project feasibility against scenarios of lower prices or higher interest rates. It may be wise to phase large projects and ensure flexibility (modular designs that can be repurposed) rather than launching everything at once. In short, avoid the overbuild trap by aligning project launches with real demand indicators.

- Innovate in Financing and Ownership Models: To keep fueling growth in a high interest rate environment, embrace innovative financing. This could mean establishing or utilizing REITs to recycle capital – sell stabilized assets into a REIT to free up cash for new developments, while earning management fees. Also consider fractional ownership or crowdfunding for projects, which can widen your investor base. In markets like Dubai, where expats are increasingly buyers, offer flexible payment plans or rent-to-own options to convert renters into buyers (this also builds loyalty and occupancy). By lowering the barriers to entry for buyers/investors, firms can sustain sales momentum even if credit is tight.

- Embrace PropTech and Sustainability for Efficiency: Make technology and sustainability core to your strategy. Use PropTech solutions – for example, digital platforms for sales can reach overseas investors and speed up transactions, and property management software can reduce operating costs for your rental portfolio. Implement Building Information Modeling (BIM) and even AI in design/construction to cut waste and delays. On sustainability, get ahead of the curve by adopting green building standards (LEED or local equivalents) in new projects; this not only prepares for future regulations but can also attract institutional investors who have ESG mandates. Energy-efficient buildings with solar panels or smart cooling can actually command higher rents from corporate tenants increasingly conscious of ESG. Essentially, future-proof assets now to maintain value in the long run.

- Strategic Urban Partnerships: Engage proactively with governments and mega-project developers. Many GCC cities have master plans (like Riyadh’s 2030 plan or Oman’s Vision 2040 tourism zones) – align your projects to these plans to ride the wave of infrastructure support. If a new metro line or airport is coming, secure land nearby early. Partner with government entities for public housing or mixed-use projects (they often provide land or financing incentives). For example, being part of transit-oriented developments around new metro stations in Doha or Dubai can ensure high footfall and demand. Also, consider cross-border expansion within GCC – as regulations unify, a developer successful in the UAE could replicate its model in Saudi or vice-versa, leveraging brand reputation. Boards should look at the GCC holistically as one market evolving, rather than siloed national markets, and position their companies to operate and compete region-wide.

Explore more insights in our blogs on NexStrat.AI.

About NexStrat AI:

NexStrat AI is at the forefront of AI and business strategy innovation. As the ultimate strategy and transformation AI co-pilot and platform, we help leaders and strategists craft winning strategies and make effective decisions with speed and confidence.

Contact Us:

Have questions or want to learn more? Contact us at [email protected]

Follow Us:

Join our community of forward-thinking business leaders on LinkedIn.