Introduction: A New Era of EBITDA Growth and Profitability in the GCC

As the Gulf Cooperation Council (GCC) enters a period of accelerated economic transformation, diversification, digitalization, and sustainability are becoming critical pillars of growth. The average EBITDA margin trends in the GCC over the recent five years offer crucial insights into how top sectors have performed and what will drive future profitability. This forward-looking perspective provides an in-depth analysis of the top five sectors in the GCC—oil & gas, real estate, banking, chemicals, and telecom—identifying key drivers, opportunities, and strategic imperatives.

The following analysis incorporates the latest insights and data, and uses the sector-level EBITDA trends to frame actionable strategies that companies in the GCC should adopt to capitalize on emerging growth opportunities.

Sector-Wise EBITDA growth in GCC and Strategic Pathways

Oil & Gas

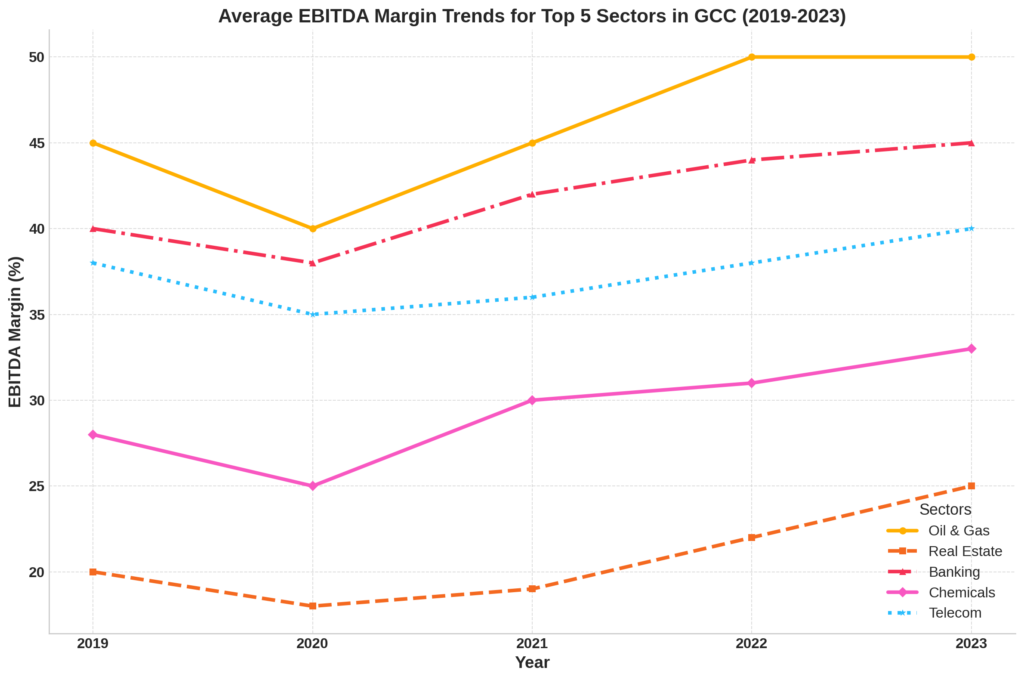

The oil & gas sector has experienced notable volatility, with EBITDA margins ranging from 40% in 2020 to 50% in 2023. This fluctuation underscores the sector’s susceptibility to global price shocks. However, oil & gas companies in the GCC are increasingly positioning themselves to play a key role in the global energy transition, particularly through investments in green hydrogen and carbon capture technologies. Countries like Saudi Arabia and the UAE are making significant strides towards becoming global leaders in low-carbon energy, and companies that embrace these technologies will enjoy not only operational cost efficiencies but also access to new revenue streams in the form of clean energy exports.

For firms that fail to pivot towards sustainability, the risk of margin erosion is high, especially as global markets and investors turn their attention toward environmentally conscious operations. Operational agility and a dual strategy that balances traditional fossil fuel extraction with investments in renewables will be critical to securing future profitability.

Real Estate

The real estate sector has shown stable but lower EBITDA growth compared to others, moving from 18% in 2020 to 25% in 2023. This average reflects the sector’s reliance on traditional infrastructure and residential property investments. However, real estate profitability is poised to increase significantly through the development of smart cities and technology-driven property solutions. Projects such as Saudi Arabia’s NEOM and the UAE’s Dubai Urban Master Plan 2040 are creating a future where digitally integrated cities will dominate, pushing EBITDA margins higher as the value proposition shifts from pure construction to technology-enabled urban living.

Developers who invest early in digital infrastructure, green building certifications, and AI-driven property management will be able to command higher margins and attract both local and international investors. The sector will need to focus on public-private partnerships to unlock the full potential of smart city projects, integrating technology to optimize urban planning, resource allocation, and energy efficiency.

Banking

The banking sector has maintained strong and consistent EBITDA margins, ranging from 40% in 2019 to 45% in 2023. This resilience is attributed to tight cost control, increased digitalization, and a favorable interest rate environment. Going forward, the sector’s profitability will be driven by the rise of embedded finance—the integration of financial services into non-banking platforms. Open banking frameworks will decentralize financial services, allowing banks to offer highly personalized, AI-driven services across industries like e-commerce, telecom, and fintech.

Banks that succeed will be those that embed themselves into digital ecosystems, using AI-driven insights to enhance customer engagement and optimize lifetime value. The next wave of growth will also come from ESG-based financing as environmental and governance criteria become more important to investors. Early adoption of green financing practices will enable banks to tap into new revenue streams while also meeting regulatory demands.

Chemicals

The chemicals sector has seen steady EBITDA margin, rising from 25% in 2020 to 33% in 2023. The sector is increasingly focusing on sustainable production and green chemistry, driven by rising regulatory demands for lower carbon emissions. The future of the chemicals sector will depend heavily on the adoption of circular economy models, where recycling and reducing waste are embedded into core operations.

Investments in bio-based chemicals and innovations in green chemistry will not only reduce costs but also provide access to premium markets, particularly in Europe, where demand for sustainable products is growing. GCC chemicals companies that take early action to transition to low-carbon production processes will be able to charge higher prices and access sustainability-linked financing, which offers more favorable terms.

Telecom

The telecom sector has seen EBITDA growth steadily from 35% in 2020 to 40% in 2023. Future growth in this sector will be driven by the rollout of 5G infrastructure and the expansion of digital services beyond traditional connectivity. As telecom operators transition into digital ecosystem enablers, they will be able to tap into new verticals such as healthcare, logistics, and smart cities.

Telecom companies will need to prioritize partnerships with industry verticals to provide tailored digital solutions that go beyond basic connectivity services. The ability to offer enterprise-grade digital solutions and AI-driven platforms will open new, higher-margin revenue streams. Companies that embrace the role of being the backbone of smart cities will see sustained EBITDA growth and enhanced profitability.

Macro-Level Strategic Imperatives for GCC Firms‘ EBITDA growth

1. Accelerating ESG Adoption: From Compliance to Competitive Advantage

As environmental, social, and governance (ESG) criteria shift from being a regulatory requirement to becoming central to corporate strategy, GCC firms must evolve their approaches to sustainability. ESG is no longer merely about meeting minimum regulatory requirements; it is a crucial driver of long-term profitability, access to capital, and market competitiveness.

Energy transition is at the heart of this shift. The global push towards net-zero emissions is forcing industries like oil & gas and chemicals to rethink their business models. Companies that integrate green energy technologies such as carbon capture, renewable energy production, and hydrogen projects will not only comply with global carbon standards but also unlock new revenue streams through sustainability-linked financing and premium pricing in eco-conscious markets like Europe.

- For the oil & gas sector, this means aggressively investing in clean energy projects such as hydrogen and solar energy to secure a foothold in the emerging green economy.

- Chemicals companies must shift towards a circular economy model, reducing waste and producing biodegradable products, which will allow them to meet both regulatory demands and market preferences for sustainable products.

- Real estate developers must focus on green building certifications and energy-efficient design, positioning themselves as leaders in sustainable urban infrastructure development, particularly as smart cities like NEOM and Dubai’s Urban Master Plan 2040 take shape.

Moreover, integrating ESG metrics into operational KPIs will help firms attract the growing pool of ESG-focused investors, who are increasingly seeking companies that can deliver both financial returns and positive environmental or social impacts. Companies that are early adopters of sustainability practices will benefit from enhanced investor confidence, lower capital costs, and stronger brand equity in a marketplace where environmental stewardship is becoming a key differentiator.

2. Expanding Digital Ecosystems: Building Beyond Connectivity and Services

The digital transformation of industries such as banking, telecom, and real estate is no longer about enhancing operational efficiency—it is now the engine of growth and competitive advantage. Companies that build digital platforms capable of offering integrated services across industries will lead in tomorrow’s economy. In the GCC, the growing adoption of Super-Apps, 5G, cloud computing, IoT, and AI is paving the way for new digital ecosystems that will transcend traditional industry boundaries.

For telecom operators, the evolution from connectivity providers to digital ecosystem enablers will allow them to tap into lucrative new verticals such as healthcare, smart logistics, and industrial IoT. By leveraging 5G infrastructure, telecom firms can provide real-time, high-speed data solutions that empower industries to optimize operations, reduce costs, and offer tailored digital services. These integrated digital ecosystems will enable telecom companies to move beyond commoditized connectivity into higher-margin, value-added services.

- Healthcare: Telecom companies can partner with healthcare providers to create telemedicine platforms, enabling remote consultations, diagnostics, and AI-powered health monitoring.

- Smart Cities: By partnering with urban developers, telecoms can offer the connectivity backbone for smart city applications, such as smart transportation, energy management, and security services.

- Logistics and Industrial Automation: Collaborations with logistics companies will allow telecom firms to provide real-time tracking, AI-based analytics, and optimized supply chain solutions.

For the banking sector, embedded finance offers a unique opportunity to integrate financial services into non-financial platforms. By partnering with e-commerce platforms, telecom companies, and retailers, banks can offer financial services—such as credit, insurance, and payment options—embedded into customers’ everyday transactions. As open banking and API-driven financial solutions gain traction, banks must focus on delivering AI-driven personalization to cater to customer needs, optimizing lifetime value and deepening customer relationships.

Real estate developers can expand their service offerings by integrating proptech into property management and development. Technologies such as AI-based property management systems, digital twins, and IoT-enabled smart buildings will allow real estate firms to differentiate themselves, increase operational efficiency, and capture higher margins. These innovations are particularly relevant as smart city projects across the GCC take off, providing ample opportunities for firms to partner with governments and tech companies.

3. Innovating for Resilience: Building Agility Through Technology and Sustainability

Innovation is no longer a luxury; it is a strategic imperative for GCC firms to build resilience and ensure long-term success in an increasingly volatile global market. The rapid adoption of AI, automation, and clean technologies at scale is transforming traditional business models and offering new ways to enhance operational efficiency and uncover growth opportunities.

For the oil & gas sector, resilience will be built through investment in energy efficiency and clean energy technologies. Companies need to prioritize R&D in hydrogen production, carbon capture, and renewable energy infrastructure. By integrating AI and automation into existing oil production and refining operations, firms can reduce costs, improve safety, and ensure that traditional operations remain competitive while transitioning to a low-carbon future.

In the chemicals sector, the focus on green chemistry and bio-based products is crucial for reducing environmental impact while remaining competitive. By investing in research and development to create eco-friendly, sustainable products, chemicals companies can access premium markets in Europe and Asia that are increasingly demanding low-carbon products.

For the banking and telecom sectors, resilience lies in embracing AI-driven personalization, data analytics, and cybersecurity. Banks that can leverage AI to offer real-time, tailored financial services and telecom operators that invest in cybersecurity infrastructure to protect their digital ecosystems will gain the trust of both regulators and consumers. Moreover, automation mostly powered by agentic AI based workflows will play a key role in reducing operational costs and increasing agility in responding to market changes.

Finally, cross-industry partnerships and collaboration will be essential for building agility. By forming strategic alliances with tech companies, start-ups, and public institutions, GCC firms across sectors can tap into new capabilities and markets, ensuring they are prepared for the disruptions that will inevitably shape the future EBITDA growth economy.

Conclusion

The future of GCC profitability lies at the intersection of technology, sustainability, and ecosystem integration. As the region accelerates its shift towards digitalization and sustainability, companies must be prepared to lead the charge by embedding ESG principles, building digital ecosystems, and investing in innovation. GCC Firms that are proactive in these areas will not only enhance their EBITDA growth but also secure a lasting competitive advantage in an evolving global marketplace.

The GCC’s transformation is not just a local or regional story—it is a global narrative of how businesses can thrive by combining resilience, innovation, and sustainability to meet the challenges of the 21st century. Those that succeed in aligning their strategies with these imperatives will be best positioned to capture the growth opportunities of tomorrow.

Explore more insights in our blogs on NexStrat.AI.

About NexStrat AI:

NexStrat AI is at the forefront of AI and business strategy innovation. As the ultimate strategy and transformation AI co-pilot and platform, we help leaders and strategists craft winning strategies and make effective decisions with speed and confidence.

Contact Us:

Have questions or want to learn more? Contact us at [email protected]

Follow Us:

Join our community of forward-thinking business leaders on LinkedIn.