This report’s evaluation, analysis, and strategic insights are powered by Nexstrat.ai. To see Nexstrat.ai in action and learn how it can enhance your strategy development and decision-making, schedule a demo at nexstrat.ai/book-a-demo.

Introduction: Redefining Value in a Transformed Real Estate Landscape

The U.S. real estate market is at a transformative juncture, where soaring mortgage rates, tightening credit, and evolving consumer preferences are converging to reshape market dynamics. Amid an environment of scarce housing inventory and a significant recalibration in commercial asset values, industry leaders must navigate the delicate balance between maximizing short-term operational resilience and strategically positioning for long-term growth. This analysis unpacks the critical trends driving the market—from record-high home prices amid declining sales to the seismic shifts in office and retail property utilization—and outlines actionable strategies for turning these challenges into opportunities. For CEOs and boards, the imperative is clear: reimagine asset portfolios, embrace technological innovations in property management, and forge dynamic stakeholder partnerships to redefine value in a rapidly evolving landscape.

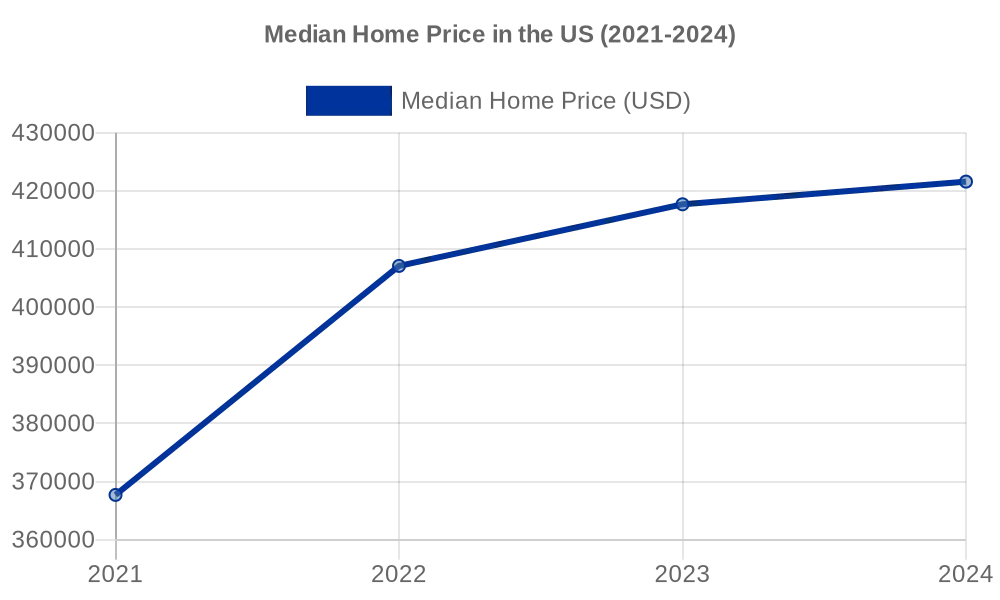

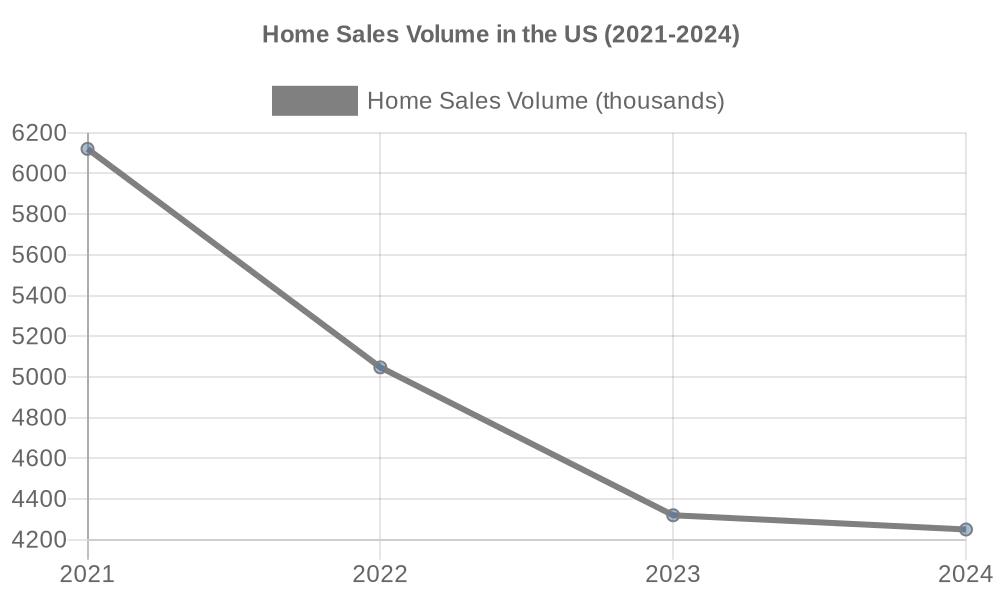

U.S. Housing Market Trends – Sales vs. Prices

Existing home sales (bars) plunged to ~4.1 million units in 2023 – a 30-year low – as 30-year mortgage rates hit ~7%, sidelining buyers. Yet the median home price (line) reached a record $407k in 2024 due to chronic supply shortages.

The U.S. real estate market has been whipsawed by the rapid rise in interest rates and shifting post-pandemic usage patterns.

Housing Market:

2023 was the worst year for home sales in over a decade, as affordability cratered. The average 30-year mortgage rate soared above 7% – up from ~3% in early 2022 (themortgagereports.com) (themortgagereports.com) – dramatically increasing monthly payments. Consequently, existing-home sales fell ~18% in 2023 to just over 4 million units (wsj.com), the lowest since the mid-1990s, aside from the brief 2008 crash. Paradoxically, home prices hit record highs nationally (reuters.com).

Why? Many owners with ultra-low mortgages chose not to sell (the so-called “golden handcuffs” of a 3% rate), leading to scarce inventory. At one point in 2024, there were barely 3 months of supply of existing homes – about half the historical norm. Bidding wars still erupted for desirable, well-priced listings, keeping prices firm even as demand languished. New home builders filled some gap by aggressively using incentives (rate buy-downs, freebies) to sell new houses, benefiting from the lack of used home competition – new home sales actually rose, and builders’ confidence rebounded by late 2023.

Commercial Real Estate (CRE):

A bifurcated story.

The office sector is in crisis: the remote/hybrid work shift has slashed demand for office space by an estimated 20-30%. U.S. office vacancy hit an all-time high around 20% in 2023 (trepp.com) (and effective occupancy is even lower, with Kastle Systems keycard data showing ~50% average workplace attendance).

Major urban office markets like San Francisco saw vacancy rates above 30% (fennemorelaw.com), resulting in plunging asset values (trophy office buildings in SF and NYC have sold at 40-60% discounts from pre-pandemic values). In contrast, industrial/logistics real estate (warehouses, distribution centers) remains robust – e-commerce growth and supply chain reconfiguration keep vacancy in single digits and rents rising, though at a slower pace than the frenetic 2021.

Retail real estate stabilized: brick-and-mortar retail sales recovered, and store openings outpaced closures in 2023 for the first time since 2016, with discount chains and experiential formats (gyms, clinics) absorbing vacated storefronts. Multifamily/apartments had a mixed year – occupancy stayed high (~95%) and rents, after a dip in late 2022, grew modestly in most markets; however, a record number of new units under construction (highest since 1970s) are coming online in 2024, which could soften rents especially in boom markets (Austin, Nashville saw slight rent declines as new supply hit (newsweek.com)).

Financial and Commercial Developments in the US Real Estate Market:

Interest Rate Impact:

Real estate is highly sensitive to financing costs, and the Fed’s rapid hikes sent shockwaves.

Property transaction volumes fell sharply (down ~60% in 2023 vs 2021 highs for commercial property sales, per Real Capital Analytics) as buyers and sellers found it hard to agree on pricing with the new borrowing costs. Cap rates (property yields) finally began rising off historic lows – but not enough yet to fully offset higher debt costs, which means many potential deals are “underwater” financially unless sellers drop prices. Lenders pulled back: banks, especially regional ones, tightened CRE lending standards to the most stringent since 2009 (reuters.com).

This credit crunch is particularly hard on office and older retail properties – refinancing these in 2024–2025 at double or triple the interest rate is often unviable. Thus, experts forecast a wave of distressed real estate sales or “hand-backs” to lenders: indeed, several marquee properties (like a NYC office tower and a LA shopping center) were simply given up by owners when loans came due, marking the first phase of distress.

Shifts in Space Demand: in the US Real Estate Market:

Corporations are rightsizing office footprints – sublease space is abundant (Seattle and SF have ~30% of office space available when including subleases). Many companies are investing in quality over quantity – upgrading to newer, amenity-rich offices to entice employees in, while exiting older buildings. This “flight to quality” means modern, green-certified offices can still lease (often at premium rents), while commodity B/C class offices languish. In retail, the shift to omni-channel means retailers want fewer but better stores – physical locations are being reimagined as showrooms or fulfillment nodes. Industrial users are demanding facilities with taller clear heights, automation features, and locations nearer to consumers to enable same-day delivery.

Residential trends:

The pandemic-driven migration (Sun Belt growth, urban outflow) moderated, but remote work continues to support high housing demand in lower-cost areas. “Zoom towns” (attractive smaller cities) still see elevated home prices. Renters in big cities gained slight bargaining power in 2023 as new apartments opened and some young folks left expensive metros, but any relief could be temporary if construction slows due to financing.

Opportunities and Risks :

Opportunities:

Adaptive reuse is a buzzword – the oversupply of offices opens the door to convert some into apartments, hotels, or labs. Cities like Washington D.C. and NYC are rolling out incentives and streamlined permitting for office-to-residential conversions. This is complex (costly retrofits, zoning hurdles) but potentially lucrative in markets with housing shortages. Industrial real estate remains a solid bet; even as e-commerce normalized, retailers are shifting from “just-in-time” to “just-in-case” inventory, keeping warehouse demand high. Also, the clean energy boom creates new real estate needs: battery and EV plants (over 100 million square feet of manufacturing space announced since 2021 in the U.S.), wind/solar farm land deals, and even carbon capture facilities – a niche but growing category – all need sites.

Risks:

If interest rates stay higher for longer, highly leveraged owners could default in greater numbers. Smaller regional banks (which hold a large share of the ~$3.2T in CRE loans) are particularly exposed to office loans; a wave of defaults could hit local economies and bank balance sheets, potentially tightening credit further (a negative feedback loop).

Regulatory changes: Some cities are contemplating office vacancy taxes or stricter rent control (to address housing affordability) – such measures could hurt values. Property taxes are rising as municipalities facing budget shortfalls target high-valued properties (even as owners argue values have fallen).

Construction costs: Though lumber and material costs came off peaks, construction is still ~20% more expensive than pre-pandemic and labor is tight, which threatens the feasibility of new projects or conversions.

Strategic Imperatives for Real Estate Industry Leaders:

Proactive Asset Portfolio Repositioning:

Whether you’re a REIT, real estate investor, or corporate real estate holder, don’t wait for pain to become crisis – act now to reshape your portfolio for the new environment. Imperative: Triage properties into keep vs. dispose categories.

For owners heavy in struggling office or older retail, consider selling non-core assets sooner at today’s prices (even if off peak), rather than risking further decline. Use any disposition proceeds to deleverage or reinvest in resilient sectors like multifamily, industrial, or “experience” retail (e.g., open-air centers with dining and entertainment).

Within your portfolio, aggressively pursue adaptive reuse opportunities: if you own a half-empty downtown office, start feasibility studies for conversion (residential, hotel, mixed-use) – engage city officials now to get support (tax abatements, zoning changes). Investors should also scout for distressed deals opportunistically: some high-quality assets with temporary distress (e.g., a luxury hotel that hasn’t recovered fully, or a top-tier office at low occupancy due to a big tenant leaving) could be acquired at discounts and turned around over a 5+ year horizon.

But be selective and ensure you have the capital reserves to carry through a possibly extended recovery. In residential development, pivot product mix toward where demand is going: single-family build-to-rent communities in the Sun Belt are hot, whereas luxury urban high-rises face more rent sensitivity.

Embrace Technology and AI/Data to Drive Performance:

The real estate sector historically lagged in tech adoption, but now it’s essential for efficiency and new revenue.

Action: Implement advanced property management systems and analytics. For landlords, utilize IoT sensors and platforms in buildings to monitor energy usage, foot traffic, air quality, etc., to optimize operations and costs. A smart building can cut energy costs by 10-20% – a key win when utilities and maintenance are big line items. Predictive maintenance analytics can prevent costly downtime for elevators or HVAC. Offer these capabilities to tenants as part of a service bundle (e.g., “green certified smart office” can command higher rent from corporates with ESG goals). In leasing, use data-driven marketing – analyze location data to understand shopping patterns for retail or commuting patterns for offices to better target prospective tenants.

Online marketplaces for leasing (like Zillow for homes, or VTS Marketplace for offices) mean quicker leasing cycles if used well. Also consider new revenue models: some landlords are monetizing data itself (aggregated pseudonymous data on visitor counts, etc., can be valuable for urban planners or retailers).

Proptech partnerships should be accelerated – whether it’s using platforms for digital tenant experience (apps that integrate access, room booking, amenity reservations) to increase satisfaction in office buildings, or deploying virtual tours and AI chatbots to lease apartments faster to Gen Z renters who avoid phone calls.

Refinancing and Capital Strategy for a High-Rate Era:

With higher-for-longer rates, a passive approach to debt can be fatal in the US real estate market.

Imperative: Proactively manage liabilities. If you have loans maturing in next 2-3 years, start refinancing discussions early. Lock in fixed rates now if you believe rates could rise more, or negotiate extensions to push maturities out, even if it comes at some cost.

Creative financing is key: explore credit tenant leases or sale-leasebacks if you’re an owner-occupier (monetize your real estate to pay down debt and lease it back). Pool and securitize attractive assets to tap CMBS or private placement markets, potentially reaching a wider investor base. Consider bringing in joint venture equity to de-risk (e.g., sell a 50% stake in a prime asset to an institutional investor to reduce your debt load).

For developers, structure deals with more equity and seek alternative financing like green bonds or PACE financing for projects that can qualify (energy-efficient projects can secure Property Assessed Clean Energy loans that have low rates). Importantly, communicate with lenders – if an asset’s NOI has fallen (e.g., an office with vacancy), present a workout plan: perhaps infusion of additional equity, a plan to redevelop or re-lease, in exchange for modified loan terms. Taking initiative can avoid fire sales and preserve long-term value.

Reimagine Space to Align with Market Needs:

The fundamental shifts in how people live, work, and shop mean the real estate product must evolve. Action: For office owners, it’s time to reinvent the office experience. Work closely with major tenants to repurpose excess space: could vacant floors become flex co-working space that you operate or partner to operate? Could part of an office building be converted to a tenant-only amenity floor with conference centers, fitness, daycare, etc., making the building a magnet for employees to come in?

Landlords should invest in hospitality-like services – concierge, curated events, tenant engagement apps – essentially treat office tenants more like hotel guests.

For retail property managers, continue shifting tenant mix towards service and entertainment – things e-commerce can’t provide. That might mean reconfiguring units (combine smaller shops into a big space for a climbing gym or a food hall). Use short-term leases or pop-ups to keep things fresh and interesting, leveraging local businesses and online-native brands that want physical presence (there’s a boom in DNVBs opening pop-up stores).

In residential, design for flexibility and community: new multifamily developments are incorporating co-working lounges (since many work from home), smart home tech, and even adaptable layouts (sliding walls, etc., to convert space as needs change). If conversions are part of your strategy, ensure the end product is appealing: simply turning an office into a bland apartment won’t cut it – engage architects to create attractive, light-filled living spaces, even if it means cutting an atrium or adding courtyards.

The bottom line: real estate no longer sells itself just by location; it must be programmed and activated to meet evolving user expectations.

Strengthen Stakeholder Relations and Navigate Policy:

In this period of stress, it’s vital to proactively manage relationships with key stakeholders – regulators, community, and tenants. Imperative: Engage local governments on solutions for vacant properties. Many cities are keen to avoid urban blight; propose win-win initiatives (e.g., you’ll convert that half-empty mall into a mixed-use community if the city provides tax incentives or helps with rezoning). Be part of downtown revival task forces if you have holdings there – your input can shape public investments (like transit improvements or safety initiatives) that directly impact property values.

On the residential side, keep a close pulse on regulatory changes like rent control expansions – join industry coalitions to present data on why such measures might reduce new housing supply. Consider voluntary measures to demonstrate goodwill: for instance, some landlords offered flexible rent payment options during tough times or participated in housing voucher programs – this can pre-empt heavier-handed regulation and build reputation. With tenants, especially commercial ones, this is the time for partnership over adversarial relationships. A struggling retailer tenant might benefit from percentage rent deals (where rent correlates with sales) – which could keep them in business and keep your center occupied.

For offices, if a major tenant is weighing downsizing, work with them – better to adjust their lease terms now and maybe extend the term than to lose them entirely next year. The goal is to maintain occupancy and cash flow, even if it means short-term concessions; a half-occupied building is far costlier to your bottom line than a fully occupied one at slightly lower rent.

US Real estate market, more than any sector, operates on lagging indicators – but forward-looking leadership is needed now to get ahead of the curve.

Call to action:

Industry leaders and investors in the US real estate market must be honest about the new fundamentals (interest rates likely stabilizing around historically normal levels, not zero; demand patterns permanently altered by technology and demographics) and adjust strategies accordingly. The easy gains of the 2010s (falling cap rates, rising leverage, ever-growing demand for all asset classes) are over. The next winners in real estate will be those who innovate and adapt – repurposing assets, adopting technology, and restructuring finances – rather than clinging to old playbooks.

Board directors should challenge management: “What is our plan for each asset category under a high-rate, hybrid-work scenario? How are we turning this into an opportunity?” Encourage bold actions like strategic mergers or acquisitions if scale will bring efficiency (e.g., consolidating property management to reduce costs, or acquiring a proptech firm to leapfrog capabilities). Ultimately, real estate remains a cyclical, location-driven business – but smart operators can create their own cycles by actively managing and not just passively owning. By executing the imperatives above, real estate leaders can stabilize their portfolios in the near term and set the foundation to rebuild value and growth as the environment eventually improves. In doing so, they will emerge from this period not only intact but with portfolios aligned to the future of living, working, and commerce.

Explore more of our insights on Nexstrat.ai.

About NexStrat AI:

NexStrat AI is at the forefront of AI and business strategy innovation. As the ultimate strategy and transformation AI co-pilot and platform, we help leaders and strategists craft winning strategies and make effective decisions with speed and confidence.

Contact Us:

Have questions or want to learn more? Contact us at [email protected]

Follow Us:

Join our community of forward-thinking business leaders on LinkedIn.