Introduction: Navigating Retail’s New Consumer Paradigm

In a landscape defined by rapid digital evolution and shifting consumer behaviors, the US retail industry stands at a pivotal crossroads. The post-pandemic world has redrawn the rules of engagement: while brick-and-mortar stores have rebounded, digital channels continue to redefine customer expectations and market share. Today’s retail leaders face a dual mandate—harness the enduring power of physical retail experiences while accelerating omnichannel innovation to meet the “value now” mindset of an increasingly discerning consumer base.

The convergence of economic headwinds—from inflationary pressures and rising interest rates to supply chain recalibrations—has forced retailers to reimagine their value propositions. Traditional sales channels are being augmented by agile e-commerce strategies, and the importance of seamless, integrated shopping experiences has never been more pronounced. Meanwhile, the resurgence of consumer in-store engagement, coupled with a nuanced approach to promotions and inventory management, underscores the imperative to build resilient, data-driven models that can adapt to market volatility.

Dynamic Forces in the US Retail Industry: A Quick Look

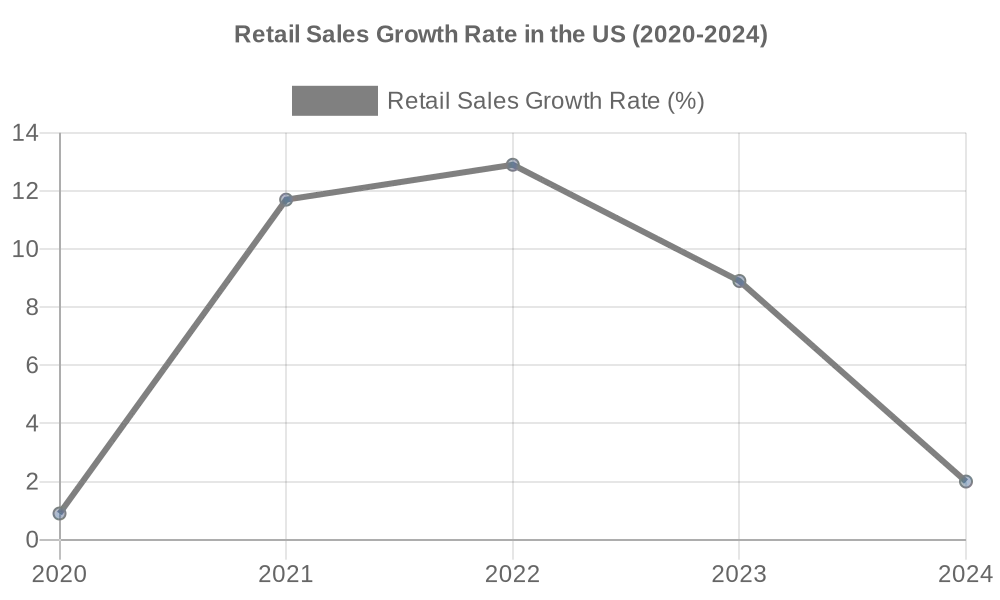

After the pandemic spike in 2020, online sales (as % of total retail) plateaued around 14–15% through 2022, then resumed climbing to ~16% in 2024 (oberlo.com.) Physical retail has rebounded, but digital channels continue to gradually expand their share. The U.S. retail sector in 2023–2024 has been a story of resilience under pressure and significant shifts in consumer behavior. Despite the highest inflation in 40 years and rising interest rates, American consumers largely kept spending: total retail and food services sales rose 3.2% in 2023 (nominal) over the prior year (moodyscre.com). However, this growth was uneven – big winners included segments like restaurants and bars (food services sales jumped +11.3% in 2023 (moodyscre.com) as consumers eagerly returned to dining out), while some goods categories (furniture, electronics) saw flat or declining volumes once adjusted for inflation. Retailers navigated a challenging dichotomy: on one hand, a strong job market and rising wages fueled consumer demand; on the other, high prices and interest costs strained wallets, forcing shoppers to become more value-conscious and selective. Early 2024 brought relief as inflation moderated to ~3–4%, but consumers remained cautious, toggling between “trading down” on everyday items and splurging occasionally – what McKinsey dubs the “value now” mindset (mckinsey.com).

Impact on the US Retail Industry:

Shifts in Consumer Behavior:

U.S. consumers emerged from the pandemic with altered habits. In 2023, they redirected spending from goods to services (travel, dining, entertainment), a normalization that hit retailers of home goods, electronics and apparel which had boomed in 2020–2021. For example, electronics retailers reported low-single-digit declines as the pandemic upgrade cycle faded. At the same time, categories like grocery and essentials saw sustained demand but with a twist – shoppers increasingly opted for store brands and discounts. Grocery chains’ private label sales grew significantly as consumers sought cheaper alternatives amid food inflation hovering ~6%. Promotional intensity ticked up across retail – after a period of low promotions due to supply shortages, retailers in late 2022 and 2023 had to clear excess inventory (especially in apparel and home goods), leading to the return of widespread markdowns.

Commercial realignment:

Brick-and-mortar stores saw foot traffic recover. Notably, U.S. mall traffic in holiday 2023 was up mid-single-digits percent versus 2022, though still below 2019. Retailers with omni-channel strength thrived: those who seamlessly integrated online and store (curbside pickup, ship-from-store) gained share. The blend of physical and digital was evident as Target’s same-day pickup sales jumped ~50% in 2023, showing consumer appetite for convenience.

Financial pressures:

With the Fed’s rate hikes, the cost of carrying inventory and operating on credit rose. Smaller retail chains with heavy debt felt the squeeze (some filed Chapter 11). Credit card interest rates above 20% and rising balances (stlouisfed.org) signaled that lower-income consumers were stretching, potentially presaging a spending pullback in discretionary categories.

Disruptions and Opportunities in the US Retail Industry:

Digital Disruption:

E-commerce’s growth in the US retail industry, while not as explosive as 2020, remains a secular trend. Online penetration ticked back up to ~15% of retail in 2023 (oberlo.com) and is projected ~17%+ by 2025. Retailers are heavily investing in logistics and tech – from same-day delivery networks to AI-driven personalization – to capture online growth and improve margins. The lines between retail and tech are blurring: Amazon’s and Walmart’s advertising businesses (monetizing their shopper data) grew to tens of billions, becoming high-margin profit engines.

Consumer Experience & Loyalty:

Post-pandemic consumers value experiences and authenticity. Brands with strong community engagement (through social media, loyalty apps) and experiential retail formats (in-store events, personalized services) are winning loyalty. For instance, Nike’s membership program, which offers exclusive drops and in-store experiences, helped drive a double-digit increase in direct sales.

Macroeconomic Risks:

A potential late-2024/2025 economic slowdown is a looming risk. Retailers could face a scenario of volume declines even if inflation cools, as higher loan/credit payments siphon discretionary income. Moreover, the resumption of student loan payments in late 2023 (after a pause) is pulling an estimated $9 billion per month from consumer spending, disproportionately impacting younger consumers’ budgets.

Inventory & Supply Chain:

The supply chain snarls of 2021–22 eased considerably by 2023; lead times normalized and import costs fell. The US retail industry learned from the chaos and are implementing more agile supply chains – diversifying sourcing (China+1 strategies, nearshoring to Mexico/Central America for faster turnaround) and using data to manage stock levels. This agility is crucial as consumer demand signals remain volatile. Many retailers now deploy AI forecasting to better align inventory with fast-changing trends (for example, a fashion retailer might use real-time social media data to predict a surge in demand for a style and avoid stockouts or gluts).

Strategic Imperatives for Retail Leaders:

- Deepen Omni-channel Integration: The future belongs to retailers in the US retail industry who can serve customers wherever they are with a unified experience. Imperative: Break down silos between e-commerce and stores – if they still exists – align pricing, promotions, and inventory across channels. Invest in technologies that provide a single view of the customer and inventory. For example, implement RFID or IoT tracking to know inventory in real time and fulfill online orders from the closest store to the customer, cutting delivery times and costs. Encourage behaviors like BOPIS (buy online, pick up in store) and BORIS (buy online, return in store) to drive cross-selling when customers visit. Make stores mini distribution centers. KPI shift: measure success in terms of overall customer lifetime value and omni-channel contribution, not just same-store sales. CEOs should champion an “omni P&L” approach, incentivizing teams to optimize the whole, not individual channels.

- Embrace the “Value + Values” Consumer: Today’s shoppers are bifurcated – they demand both value for money and alignment with their values. Action: Adjust product assortments and marketing to reflect this dual desire. On value: Ensure a strong private label offering (with quality near national brands) to capture trade-down shoppers – grocery chains have done this, but apparel and others can expand into essentials lines. Leverage data to tailor promotions; use loyalty program insights to target discounts to price-sensitive cohorts while preserving margin on less sensitive ones. On values: Emphasize sustainability and social responsibility in the assortment. For instance, a fashion retailer might commit to using 50% recycled materials by 2025 and market a collection as “eco-friendly” which can command premium pricing even in tight times. Transparent messaging about sourcing (fair trade, carbon footprint) and community give-back programs can differentiate your brand. Retailers like Patagonia thrived by appealing to values – find your brand’s authentic stance and amplify it.

- Optimize Costs with Tech and Partnerships: Margin pressure in retail is constant, so attacking structural costs is key. Imperative: Deploy automation and augmentation -both with AI – consider automated fulfillment centers (as seen in Amazon’s robotics), electronic shelf labels for dynamic pricing, and AI-driven planogram optimization to maximize sales per square foot. Also, assess your store footprint: many chains are rightsizing – closing underperforming stores while opening smaller format or concept stores in promising markets. Negotiate rents aggressively or explore revenue-share models with mall landlords as traffic patterns change. On partnerships: collaborate with tech firms and even competitors where it makes sense. For example, join delivery consortiums to share logistics costs in last-mile delivery, or partner with marketplace platforms to extend your online reach without heavy capex. Another opportunity is retail media networks – if you have significant traffic (online or in-store), monetize it by selling ad placements or data insights to suppliers (nasdaq.com), which directly adds to profit.

- Enhance Customer Engagement through AI : In a world of fickle loyalty, proactively engaging customers is critical. Action: Adopt an AI first approach to personalize interactions at scale. Use your loyalty program not just as a rewards system but as a rich data source – analyze the top 10% of customers who drive ~40% of sales (typical in retail) and devise VIP experiences for them (early access to sales, exclusive products). Additionally, invest in community-building: brands like Glossier achieved cult status by fostering customer communities online. Engaged customers are more resilient in sticking with you during downturns.

- Supply Chain Agility and Localization: The pandemic taught hard lessons about over-reliance on distant suppliers. Retailers must continue to build agility. Imperative: Diversify sourcing geographically to mitigate risks – for instance, shift a portion of production to Latin America or South-East Asia from China to reduce tariffs and transit time. Closer to home, explore “made in USA” or local artisan product lines; these can cater to the conscious consumer and shorten lead times. Implement contingency plans with tier-2 and tier-3 suppliers; don’t just rely on your immediate vendors. Use demand sensing tools (AI that predicts demand surges/drops) to adjust orders quickly – e.g., if a certain apparel trend spikes on TikTok, be prepared to expedite additional stock via air freight if needed, and conversely, have cancellation clauses for predicted slow-movers. Finally, ensure last-mile delivery can flex: in urban areas, secure multiple delivery partners (traditional carriers plus gig-economy services) so capacity can scale during peaks without crushing your customer promise. The goal is a supply chain that’s as dynamic as the market itself.

For retail executives, the stakes in 2025 are high: consumers have more choices and more constraints than ever. The winners will be those who listen intently to the customer and innovate fearlessly in response. This means creating a retail experience that is convenient, affordable, and aligned with customers’ lifestyle values. Strategically, retail CEOs and boards should view the current landscape as an inflection point – an opportunity to trim the fat, solidify loyalty, and capture share as weaker players falter.

Call to action:

Make bold moves now. Whether it’s a transformative AI investment, a radical collaboration, or a reinvention of your value proposition, now is the time to position your retail business not just to survive, but to thrive in the post-pandemic, high-interest rate world. Retail has always been about evolution – those who evolve fastest now will lead the pack in the years ahead.

Explore more of our insights on Nexstrat.ai.

About NexStrat AI:

NexStrat AI is at the forefront of AI and business strategy innovation. As the ultimate strategy and transformation AI co-pilot and platform, we help leaders and strategists craft winning strategies and make effective decisions with speed and confidence.

Contact Us:

Have questions or want to learn more? Contact us at [email protected]

Follow Us:

Join our community of forward-thinking business leaders on LinkedIn.